ETF Trading Strategy Using Quarterly Institutional Adjustment Patterns

- Nov 28, 2025

- 9 min read

Updated: Dec 1, 2025

ETF trading strategy becomes dramatically more effective when built around quarterly institutional adjustment patterns rather than technical indicators or momentum signals. Most traders develop strategies based on moving averages, RSI, or candlestick formations without understanding that large institutional money operates on mechanical quarterly schedules that create predictable sector rotation opportunities. Success emerges from recognizing that pension funds, mutual funds, and endowments must restore target allocations every quarter regardless of market conditions, creating systematic windows when specific sector ETFs experience buying or selling pressure.

The challenge with traditional ETF trading strategy lies in timing entries and exits based on lagging indicators that respond to price movements after institutional positioning is complete. By the time technical signals confirm momentum, institutional flows have often peaked and reversal risk increases significantly. Professional strategies anticipate these quarterly adjustment windows by tracking which sectors have moved furthest from target allocations, then position ahead of the mechanical flows that must occur as March 31, June 30, September 30, and December 31 approach.

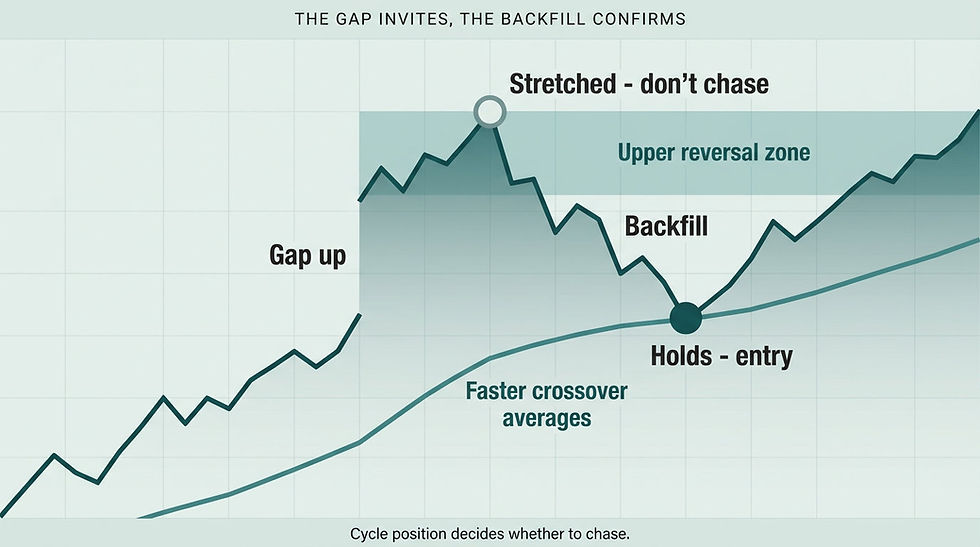

Market Turning Points teaches a comprehensive ETF trading strategy that prioritizes quarterly institutional calendar awareness over indicator-based timing. Rather than reacting to technical signals generated from past price action, this approach identifies when institutional capital must flow into specific sectors based on prior quarter performance and allocation mandates. Price channels confirm optimal entry timing, while crossover signals validate that anticipated institutional participation is materializing in observable trading activity.

Understanding Quarterly Adjustment Mechanics in ETF Trading Strategy

Quarterly adjustment cycles create the foundation for systematic ETF trading strategy because these patterns repeat predictably every three months with mechanical precision. Institutional mandates require funds to maintain specific sector allocation percentages, forcing adjustments when market performance causes drift from target weights. When technology outperforms significantly during a quarter, institutions holding 20% technology allocations may find themselves at 25% by quarter-end, requiring systematic selling to restore the mandated 20% target regardless of momentum or fundamental outlook.

This mechanical behavior provides clear timing windows for ETF trading strategy development. The final two weeks of each quarter concentrate institutional adjustment activity as large funds execute allocation restorations simultaneously. Sector ETFs that outperformed face selling pressure as institutions reduce overweight positions, while underperforming defensive sectors experience buying as funds restore minimum allocation requirements. These flows occur independently of economic data, earnings reports, or market sentiment, creating opportunities for traders who understand institutional calendar constraints. Check our post on Volatility Decay and Why Leveraged ETFs Multiply Losses During Declines for more info.

Price Channel Integration for Quarterly Window Timing

Price channels transform quarterly institutional awareness into actionable ETF trading strategy by revealing when sectors reach boundaries that trigger adjustment flows. When a growth sector ETF trades at the upper boundary of its established channel heading into the final two weeks of a quarter, this combination signals probable institutional selling regardless of recent performance or positive news. The upper channel boundary represents maximum institutional positioning that cannot be sustained through mandatory quarterly adjustments back to target allocations.

Conversely, defensive sector ETFs at lower channel boundaries approaching quarter-end indicate optimal entry timing as institutional buying pressure must emerge to restore minimum allocation levels. Healthcare, utilities, or consumer staples ETFs that underperformed during a quarter face mechanical institutional purchases in the final adjustment window even if fundamental outlook appears negative. This systematic approach to ETF trading strategy removes prediction from the equation, replacing subjective market calls with objective institutional calendar analysis confirmed through price structure positioning. Check our post on Professional Swing Trading vs Day Trading: How Institutional Timing Patterns Favor Multi-Day Positions for more info.

Sector Rotation Patterns Within Quarterly Cycles

ETF trading strategy optimization requires understanding which sector rotations repeat most reliably within quarterly institutional adjustment windows. Growth versus defensive rotation creates the most consistent pattern, with technology, consumer discretionary, and financial sectors experiencing selling pressure when they outperform during quarters, while utilities, consumer staples, and healthcare face buying when they underperform. This rotation occurs mechanically as institutions restore balanced allocations rather than making directional market bets.

International versus domestic rotation also follows quarterly patterns based on relative performance and currency movements. When international developed or emerging market ETFs outperform U.S. large-cap funds during a quarter, adjustment selling creates opportunities in those international positions while domestic buying emerges. Bond versus equity allocation adjustments create additional opportunities as institutions restore target fixed income percentages after equity market moves change overall portfolio weights. Understanding these recurring rotation patterns elevates ETF trading strategy from random sector selection to systematic institutional flow capture. Check our post on Warren Buffett Cash Position Strategy: Why 340 Billion Signals Market Cycle Discipline for more info.

Combining Quarterly Windows with Federal Reserve Meeting Cycles

Advanced ETF trading strategy combines quarterly adjustment awareness with Federal Reserve meeting timing for enhanced opportunity identification. When Fed meetings occur within the final two weeks of quarters, defensive sector rotation ahead of policy announcements amplifies quarterly adjustment buying in those same defensive sectors. Growth sectors face both pre-Fed defensive rotation and quarterly adjustment selling simultaneously, creating particularly strong downward pressure that provides optimal entry timing for patient traders.

Conversely, when Fed meetings conclude shortly after new quarters begin, growth sector buying pressure combines institutional fresh capital deployment with post-Fed risk-on rotation. These multi-factor confluences create the highest-probability setups in systematic ETF trading strategy by ensuring multiple institutional flows move in the same direction simultaneously. Understanding how quarterly cycles interact with Fed meeting patterns separates advanced strategy development from simple calendar awareness.

People Also Ask About ETF Trading Strategy

What makes quarterly institutional adjustment patterns effective for ETF trading strategy?

Quarterly institutional adjustment patterns provide effectiveness for ETF trading strategy because these flows occur mechanically based on mandate requirements rather than discretionary investment decisions. When pension funds exceed target allocations in growth sectors, they must sell regardless of momentum, fundamentals, or market sentiment. This mandatory behavior creates predictable windows when sector ETFs experience pressure unrelated to company performance or economic conditions. Traders who position ahead of these adjustment windows capture institutional flows rather than competing against them through momentum chasing.

The predictability of quarterly dates (March 31, June 30, September 30, December 31) allows systematic strategy development around known institutional calendar constraints. Unlike economic data releases or earnings seasons that create unpredictable volatility, quarterly adjustment windows repeat with mechanical precision every three months. ETF trading strategy built around these patterns generates consistency because institutional behavior follows mandates that don't change based on market conditions, creating reliable opportunities that persist across all market environments and economic cycles.

How do price channels improve quarterly adjustment timing in ETF trading strategy?

Price channels improve quarterly adjustment timing by revealing when sector ETFs reach positioning extremes that trigger institutional flows. An ETF trading strategy using channels identifies upper boundaries where sectors have become overweight and face mandatory selling pressure approaching quarter-end. Lower boundaries indicate where underweight sectors will experience institutional buying to restore minimum allocations. These visual reference points transform calendar awareness into specific entry and exit timing without requiring complex indicator calculations or subjective interpretation.

Channel boundaries also provide clear risk management parameters for ETF trading strategy implementation. Stops placed below lower channel boundaries during anticipated buying windows protect capital if institutional flows fail to materialize as expected. Exits at upper channel boundaries before quarter-end prevent holding through predictable adjustment selling that often reverses recent gains. This systematic approach to position management removes emotional decision-making while ensuring trades align with institutional flow probabilities rather than hoping for continued momentum regardless of adjustment timing.

Can ETF trading strategy based on quarterly patterns work in all market conditions?

ETF trading strategy based on quarterly institutional adjustment patterns works effectively across all market conditions because mandate requirements persist regardless of bull or bear markets. Institutions must restore target allocations whether markets are rising or falling, creating sector rotation opportunities during both positive and negative periods. During bull markets, quarterly adjustments rotate profits from outperforming growth sectors into underperforming defensive positions. During bear markets, adjustments rotate capital from oversold defensive sectors back into growth positions that have declined below target allocations.

The key to consistent ETF trading strategy results lies in recognizing that quarterly flows create relative opportunities between sectors rather than absolute market direction calls. A technology ETF may decline during quarterly adjustment selling in both bull and bear markets, but the pattern remains consistent regardless of overall market environment. Defensive sector buying during adjustment windows occurs whether markets are strong or weak. This relative rotation framework allows strategy implementation that captures institutional flows without requiring accurate market timing or economic forecasting ability.

How far in advance should ETF trading strategy position for quarterly adjustments?

ETF trading strategy should begin positioning approximately two to three weeks before quarter-end dates to capture institutional flows as they develop. Waiting until the final week often means missing optimal entry prices as adjustment pressure builds gradually rather than occurring suddenly on the last day. Early positioning at price channel boundaries during the three-week window before quarter-end provides better risk-reward ratios by entering before the heaviest institutional flow concentration occurs.

However, positioning too early (four or more weeks before quarter-end) risks holding through continued momentum in the opposite direction before adjustment flows materialize. Growth sectors may continue rallying into the final month of quarters before adjustment selling emerges. Defensive sectors may continue weakening until the final weeks when institutional buying begins. The two to three week window balances early positioning advantages against the risk of premature entries before institutional flows actually begin. Monitoring price channel position during this window provides confirmation that anticipated institutional participation is starting to materialize.

What position sizing works best for quarterly adjustment ETF trading strategy?

Position sizing for quarterly adjustment ETF trading strategy should scale based on setup quality and confluence of factors. Single-factor setups where only quarterly timing aligns (without price channel confirmation or Fed meeting amplification) warrant smaller position sizes of 2-3% of capital. Two-factor setups combining quarterly timing with price channel boundaries or crossover confirmation justify moderate 3-5% positions. Three-factor confluences where quarterly windows, channel boundaries, and Fed meeting cycles align simultaneously support larger 5-7% positions.

Maximum position sizing should never exceed 10% of capital in any single sector ETF regardless of setup quality, ensuring diversification protects against incorrect analysis or unexpected market events that invalidate quarterly patterns. Spreading capital across multiple sector opportunities during quarterly windows provides better risk management than concentrating in single positions. As positions move favorably after institutional flows materialize, trailing stops at price channel levels protect profits while allowing continued gains if institutional participation exceeds expectations. This systematic position sizing approach matches capital commitment to setup probability while maintaining consistent risk management across all quarterly cycles.

Resolution to the Problem

Most ETF trading strategy approaches fail because they rely on technical indicators or momentum signals that lag institutional positioning rather than anticipating quarterly adjustment flows. This reactive framework leads to buying sector ETFs after institutional accumulation is complete and selling after rotation has already occurred. The systematic solution lies in calendar-based quarterly awareness combined with price channel confirmation that positions ahead of predictable institutional flows rather than responding to them after price movements validate patterns.

The Market Turning Points methodology provides a complete ETF trading strategy framework built around quarterly institutional adjustment calendars. By understanding which sectors face selling pressure from prior quarter outperformance and which sectors will experience buying to restore allocations, traders identify high-probability opportunities weeks before adjustment windows. Price channel analysis confirms optimal entry and exit timing, while crossover signals validate that anticipated institutional participation is materializing in observable trading activity.

Join Market Turning Points

Market Turning Points delivers comprehensive training on developing ETF trading strategy around quarterly institutional adjustment patterns rather than lagging technical indicators. Members receive detailed quarterly calendars marking institutional adjustment windows, sector performance tracking showing which positions face adjustment pressure, and price channel analysis identifying optimal entry timing. This systematic framework removes guesswork from strategy development by replacing predictions with objective institutional flow analysis.

The service provides ongoing education on combining quarterly awareness with Federal Reserve meeting cycles, seasonal patterns, and cross-asset relationships that amplify institutional flows. Members learn position sizing appropriate to setup quality, risk management through price channel stops, and trade management through complete quarterly cycles. Transform your ETF trading strategy from reactive indicator-based timing to systematic institutional flow anticipation, join Market Turning Points and start capturing quarterly adjustment patterns.

Conclusion

ETF trading strategy using quarterly institutional adjustment patterns provides systematic opportunities by positioning ahead of predictable mandatory flows rather than reacting to technical indicator signals. Understanding that institutions must restore target sector allocations every quarter regardless of momentum or fundamentals creates a reliable framework for identifying when specific sector ETFs will experience buying or selling pressure. When combined with price channel confirmation and crossover validation, this approach generates consistent results across all market conditions.

Success with quarterly adjustment ETF trading strategy requires recognizing that institutional money operates on mechanical mandate schedules creating observable patterns. Market Turning Points teaches this complete systematic approach, helping traders develop strategies that anticipate institutional flows rather than chase performance after opportunities pass. The most effective ETF trading strategy emerges from calendar-based institutional analysis and price structure confirmation, not from predicting market direction through economic forecasts or lagging technical indicators.

Author, Steve Swanson