Volatility Decay and Why Leveraged ETFs Multiply Losses During Declines

- Oct 23, 2025

- 11 min read

Volatility decay is the hidden mathematical reality that destroys leveraged ETF returns during market declines, multiplying losses far beyond what single-beta exposure would create. When TQQQ dropped nearly 50% during the April correction while QQQ lost only 17%, that wasn't bad luck or market manipulation - that was volatility decay in action. Every drop gets multiplied by leverage, and each recovery starts from a lower base, making it harder to regain ground. A 50% loss requires a 100% gain just to break even, which is why holding leveraged positions through declining cycles compounds disaster rather than temporary setback.

Leveraged ETFs can look like easy money when markets run higher, doubling or tripling daily gains and turning bursts of cycle strength into amplified profits. But the same mathematical forces that multiply gains on the way up also compound losses the moment prices slip. This isn't a flaw in the product - it's how daily rebalancing mathematics work when volatility increases. Time and turbulence erode leveraged returns during declining cycles because the compounding effect works against you instead of for you.

Understanding volatility decay means recognizing why discipline around when to use leverage and when to move to cash isn't optional caution - it's mathematical necessity. Leverage during confirmed uptrends, cash during declines, stops on every signal. That simple rule separates consistent compounding from slow erosion or catastrophic drawdown.

How Daily Rebalancing Creates Volatility Decay in Leveraged Positions

Volatility decay occurs because leveraged ETFs rebalance daily to maintain their target multiple, which creates compounding losses during volatile or declining periods. When markets swing up and down rather than trending smoothly, the daily reset mechanism forces the fund to buy high and sell low repeatedly. Each day's losses compound on a smaller base while each day's gains compound on whatever remains after previous losses.

Consider a simple example: if an investment drops 10% then rises 10%, you don't break even - you're down 1%. Apply 3x leverage to that same pattern, and you drop 30% then rise 30%, leaving you down 9% instead of 1%. The larger the swings and the longer the volatility persists, the more decay accumulates even if the underlying index eventually recovers to breakeven.

This mathematical reality is why TQQQ can underperform dramatically during corrections. The April decline didn't just triple the QQQ's 17% loss - it created a 50% drawdown because volatility was elevated throughout the decline. Multiple large daily swings, each rebalanced at 3x leverage, compounded losses faster than a simple 3x multiplier would suggest.

Recovery from volatility decay requires disproportionate gains because you're recovering from a deeper hole. After the April correction, it took more than four months of steady upside for TQQQ to finally recover and pull ahead again, even though QQQ recovered much faster. That lost time represents opportunity cost - capital trapped in recovery that could have been redeployed at better entry points.

Why Holding Through Declines Amplifies Volatility Decay Damage

The critical mistake traders make with leveraged ETFs is holding through declining cycles, which transforms volatility decay from theoretical risk to realized catastrophe. When cycles begin rolling over and price structure deteriorates, every day held in leveraged exposure compounds losses at an accelerating rate. The mathematics don't care about your conviction or whether you believe the decline is temporary - daily rebalancing multiplies losses regardless of your opinion.

Steve's April TQQQ example illustrates this perfectly. Anyone who bought at the start of the year and held through the correction watched triple upside gains turn into triple downside losses. The decline wasn't gradual enough to provide multiple exit opportunities - it was sharp enough that holding even a few extra days after cycles warned meant significantly deeper losses.

This is why moving to cash early, not late, is the only rational approach to leveraged positions. Waiting for certainty that a decline is real rather than temporary guarantees you'll exit after substantial damage has already occurred. By the time most traders admit the decline is serious, volatility decay has already compounded losses to painful levels.

The alternative - protecting positions with systematic exits using cycle signals and crossover levels - prevents volatility decay from accumulating. Taking small losses or even small gains when early warning signals trigger preserves capital for redeployment when cycle structure confirms recovery. For traders seeking to understand how leadership dynamics affect volatility and sector rotation during these critical transition periods, the analysis in QQQ vs SPY Performance: Why Narrow Leadership Still Drives Broad Opportunity provides additional context.

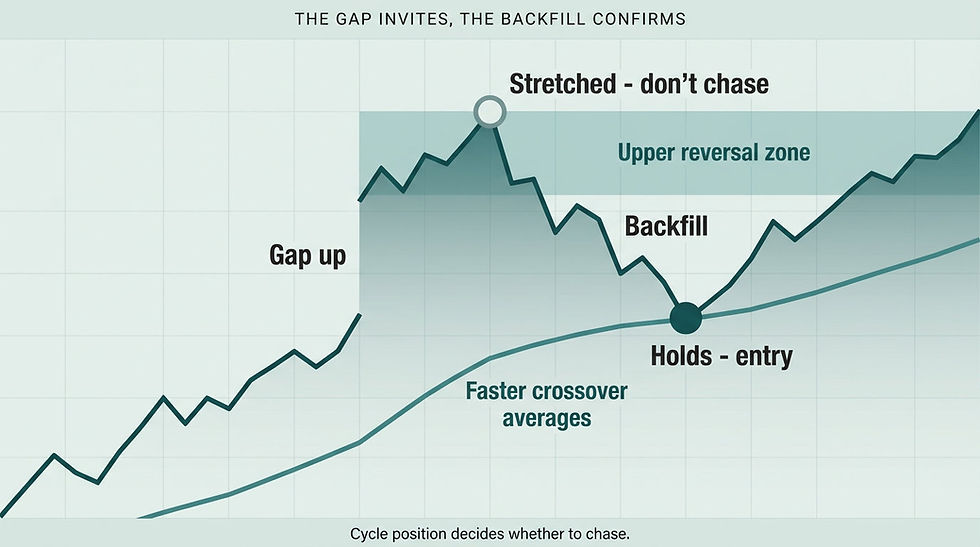

Using Layered Crossover Stops to Prevent Volatility Decay Accumulation

Volatility decay can't harm you if you're not holding leveraged positions during declining or choppy cycles, which is why systematic exit signals are essential rather than optional. The 2/3 crossover provides the first exit signal after initial entries - tight enough to lock in small gains or prevent small losses from becoming large ones. This early warning system removes you if the market isn't fully ready to run, preventing exposure during the uncertain period when volatility decay starts accumulating.

Once a rally strengthens and cycle structure confirms uptrend, protection expands by using deeper crossovers to trail positions. The 3/5 crossover allows profits to run while still protecting against meaningful reversals. Later, adding a 4/7 crossover locks in even stronger moves while giving established trends room to consolidate normally without triggering exits on minor pullbacks.

This layered structure removes emotion and replaces guesswork with process: protect first, allow profits to run second. The goal isn't maximizing every point of upside - it's keeping the math on your side by preventing opportunities from turning into setbacks through volatility decay. Each crossover layer serves specific purpose based on how far the trend has developed and how much profit needs protection.

Yesterday's profit-taking came stronger than expected because volatility remains elevated during early trend development. That's a reminder that leverage works both for and against you - small pullbacks in the underlying index become large swings in leveraged positions. The layered stop approach would have either kept you in cash awaiting clearer confirmation, or exited quickly as the 2/3 crossover broke, preventing amplified exposure to the decline. Understanding when cycle structure supports holding through normal consolidation versus exiting before volatility decay compounds is explored in Stock Consolidation Meaning in a Bullish Cycle: A Setup Not a Signal to Exit.

The Discipline of Leverage Only During Confirmed Uptrends

Volatility decay makes leverage a tool for confirmed uptrends only, not a permanent portfolio allocation or a way to compensate for uncertain timing. When cycles are rising, momentum is confirmed, and trend structure is clear, leverage amplifies the move and accelerates returns. That's when it works for you because gains compound on gains with minimal volatility decay offsetting the multiplication effect.

But the moment cycle structure shows warning signs - intermediate cycles rolling over, momentum weakening, crossovers breaking - leverage must come off immediately. Not when you're certain a decline is starting, not when the pain becomes unbearable, but when the first systematic signal triggers. This discipline is what separates consistent compounding from slow erosion.

The rule is simple: leverage during confirmed uptrends, cash during declines, stops on every signal and every uptrend. This isn't caution or fear - it's mathematical recognition that volatility decay will destroy returns if given opportunity. Markets projecting bullish uptrends into month end create the environment where leverage makes sense, but only if protection is already in place before the first sign of trouble.

Most traders learn about volatility decay the hard way - by experiencing it. The better path is learning through observation of historical examples like the April TQQQ decline, then implementing systematic protection before needing it. The math is unforgiving: a 50% loss requires 100% gain to recover. Preventing the 50% loss through disciplined exits is far easier than generating the 100% gain needed to recover from it. For comprehensive guidance on avoiding the timing mistakes that expose traders to unnecessary volatility decay, the framework in Swing Trading ETFs With Cycle Timing: How to Avoid Late Entries Near Market Tops shows how cycle context prevents both premature and late entries.

People Also Ask About Volatility Decay

What is volatility decay in leveraged ETFs?

Volatility decay is the erosion of returns that occurs in leveraged ETFs due to daily rebalancing during volatile or declining markets. Leveraged ETFs reset their exposure each day to maintain their target multiple (2x, 3x, etc.), which creates a compounding effect that works against investors when prices swing rather than trend smoothly.

The mathematics are straightforward but brutal. If an underlying index drops 10% then rises 10%, the index is down 1% overall. A 3x leveraged version drops 30% then rises 30%, leaving it down 9% instead of 1%. The larger and more frequent the swings, the more decay accumulates even if the underlying index eventually breaks even.

This decay accelerates during declining markets because losses compound on progressively smaller bases while recoveries must work harder to regain ground. A 50% loss in a leveraged position requires a 100% gain just to return to breakeven, which is why holding through corrections can take months to recover even when the underlying index bounces back relatively quickly.

Why do leveraged ETFs lose more than 3x during declines?

Leveraged ETFs can lose significantly more than their stated multiple during declines because daily rebalancing compounds losses at an accelerating rate when volatility is elevated. The 3x multiple applies to daily returns, not cumulative returns over longer periods. During sharp declines with large daily swings, the compounding effect of daily resets creates losses that exceed simple multiplication.

The April TQQQ decline demonstrates this clearly. While QQQ lost 17%, TQQQ dropped nearly 50% - far more than 3x the underlying index decline. This occurred because each day's leveraged loss reduced the base for the next day's calculation, while elevated volatility meant large swings both up and down that compounded against the position rather than for it.

Additionally, elevated volatility means the fund experiences larger intraday swings that must be rebalanced even if the index ends the day relatively flat. These intraday rebalancing costs accumulate as drag on returns that doesn't exist in the underlying index, further amplifying losses beyond the stated leverage multiple during turbulent periods.

How long does it take to recover from volatility decay?

Recovery time from volatility decay depends on both the depth of losses and the subsequent volatility of the recovery period. A leveraged position that loses 50% needs to gain 100% just to break even - a mathematical reality that makes recovery slow even when the underlying index recovers quickly. After TQQQ's April decline, it took more than four months of steady upside to finally recover and pull ahead again, even though QQQ recovered much faster.

The recovery challenge is compounded if volatility remains elevated during the rebound period. If the underlying index recovers through choppy, volatile trading rather than smooth trending, volatility decay continues accumulating even during the recovery, further extending the time needed to regain losses. Only when volatility settles and trending conditions return can leveraged positions recover at rates closer to their stated multiples.

This is why the opportunity cost of holding through declines is so severe. Capital trapped recovering from deep losses could have been redeployed at better entry points during the actual recovery phase, when cycle structure confirmed uptrend rather than attempting to time the exact bottom while suffering volatility decay throughout.

Can you avoid volatility decay with better timing?

Yes - volatility decay can be completely avoided through disciplined timing that limits leveraged exposure to confirmed uptrends and exits immediately when cycle structure shows warning signs. The key is recognizing that volatility decay only occurs when you're holding leveraged positions during declining or choppy cycles. If systematic signals remove you before significant decline begins, you never experience the compounding losses.

The layered crossover approach provides this protection. Using the 2/3 crossover as early exit signal prevents small losses from becoming large ones through volatility decay. Expanding to 3/5 and 4/7 crossovers as trends mature allows profits to run while maintaining protection against reversals. This systematic structure removes emotion - when crossovers break, positions close regardless of opinion about whether decline will continue.

Perfect timing is impossible, but avoiding the worst effects of volatility decay is achievable through discipline. Taking small losses or even small gains when early warnings trigger preserves capital for redeployment when cycle structure confirms the next uptrend, preventing both the deep drawdowns and extended recovery periods that volatility decay creates.

Should you ever hold leveraged ETFs long-term?

No - leveraged ETFs are designed as short-term trading tools for confirmed trends, not long-term holdings. The daily rebalancing mechanism that creates leverage also creates volatility decay that will erode returns over extended periods even in generally rising markets. Any period of consolidation, correction, or elevated volatility will compound losses faster than subsequent gains can recover them.

The historical data is clear: holding leveraged ETFs through complete market cycles produces returns well below what the stated multiple would suggest, and often produces losses even when the underlying index gains over the same period. This isn't a flaw in the product - it's the mathematical reality of daily rebalancing during anything other than smooth, sustained trends.

The correct use is leverage during confirmed uptrends, cash during everything else. When cycle structure shows short-term, intermediate, and long-term alignment with momentum confirmation, leverage amplifies gains effectively. When any of these components shows weakness or volatility increases, immediate exit to cash prevents volatility decay from accumulating. This requires active management - daily or at minimum weekly assessment of cycle structure and crossover positioning - which is why leveraged ETFs are tools for active traders, not passive investors.

Resolution to the Problem

The solution to avoiding volatility decay destruction isn't abandoning leverage - it's implementing systematic discipline that limits leveraged exposure to confirmed uptrends and exits immediately when structure weakens. Right now markets project bullish uptrends into month end, creating conditions where leverage can work effectively. But yesterday's profit-taking came stronger than expected, a reminder that volatility remains elevated and leverage cuts both ways.

The framework is straightforward: use the 2/3 crossover as early exit signal after initial entries, expand to 3/5 crossover as rallies strengthen, and add 4/7 crossover to lock in established moves. This layered structure protects against volatility decay accumulation by removing exposure before compounding losses develop. Taking small exits when early signals trigger prevents the 50% losses that require 100% gains to recover.

Markets will continue cycling between confirmed uptrends where leverage amplifies returns and declining or choppy phases where volatility decay destroys them. The difference between traders who compound gains consistently and those who suffer slow erosion is simple: leverage during confirmed uptrends, cash during everything else, stops on every signal. That's not caution - it's mathematical necessity.

Join Market Turning Point

Understanding volatility decay through systematic risk management isn't intuitive - it's learned discipline that replaces hope with process. Steve teaches this framework through daily market analysis showing exactly when cycle structure supports leveraged exposure and when immediate exit to cash prevents volatility decay accumulation. You're not learning to predict when declines will start - you're learning to read when protection signals trigger and exit without emotion or debate.

The difference between traders who suffer catastrophic drawdowns through volatility decay and those who compound gains consistently is framework. When you know cycle structure confirms uptrends, crossover levels provide exit signals, and leverage is tool for specific conditions rather than permanent allocation, volatility decay can't harm you because you're never exposed during periods when it accumulates.

Markets will continue creating opportunities for leverage to amplify gains during confirmed trends and destroying accounts that hold through declines. With systematic signals showing when conditions support leverage and when immediate exit prevents decay, you trade with mathematical advantage rather than hope. Discover how Market Turning Point implements systematic protection against volatility decay.

Conclusion

Markets don't reward conviction about leveraged positions held through declines - they multiply losses through volatility decay that compounds faster than most traders understand until experiencing it. When TQQQ lost 50% while QQQ declined 17%, that wasn't market manipulation - that was daily rebalancing mathematics amplifying losses during elevated volatility. The recovery taking over four months while QQQ recovered faster demonstrates the time cost of volatility decay beyond the immediate loss.

The solution isn't avoiding leverage - it's using it only during confirmed uptrends with systematic exits when first warnings trigger. The 2/3 crossover provides early protection, the 3/5 allows profits to run, the 4/7 locks in established moves. This layered structure prevents volatility decay from accumulating because positions close before compounding losses develop.

Leverage during confirmed uptrends, cash during declines, stops on every signal. That simple rule separates consistent compounding from catastrophic drawdown. Markets projecting bullish into month end create conditions where leverage works, but only if protection is already in place before needing it. The math is unforgiving - a 50% loss requires 100% gain to recover, making prevention through systematic exits far easier than recovery through hope.

Author, Steve Swanson