Time to Market: How Fed Cycle Analysis Shows When Institutions Position Before Headlines

- Oct 29, 2025

- 10 min read

When traders ask about time to market, they're really asking when to position capital for maximum advantage. The answer doesn't come from Fed meeting headlines or Powell's press conference tone. Time to market comes from reading the 30-trading-day Fed cycle within the context of intermediate and long-term rhythms. These cycles show where institutional money positions before volatility arrives, not after announcements move prices.

Fed meetings create predictable volatility windows every 30 trading days, yet this rhythm doesn't create market direction. The intermediate cycle determines whether Fed-driven volatility breaks higher or lower. The 30-day pattern simply amplifies whatever trend already exists. Understanding this relationship separates traders who react to headlines from those who position ahead of them.

Most traders confuse signal with noise around Fed meetings. Powell's dovish or hawkish tone generates short-term price movement that feels significant in the moment. Yet this tone rarely changes the underlying cycle direction. Institutions ignore the theater because they've already positioned based on where cycles sit relative to projected paths.

This article shows how cycle analysis reveals institutional positioning windows before Fed announcements. You'll learn why meeting tone matters less than intermediate cycle structure. You'll understand how the 30-trading-day rhythm amplifies existing trends rather than creating new ones. Most importantly, you'll see which crossover signals confirm time to market entries when policy volatility aligns with systematic timing.

Why Fed Meeting Tone Creates Noise While Cycles Show Direction

Markets price in expected Fed decisions weeks before announcements through futures positioning and options flow. A quarter-point cut surprises no one when derivatives markets show 95% probability of that exact outcome. What creates volatility isn't the policy decision itself but whether Powell's language suggests more cuts ahead. Retail traders parse every word searching for directional clues while institutional desks already positioned weeks earlier based on cycle structure.

Short-term traders react to tone because they lack systematic frameworks for reading what comes next. They watch for dovish or hawkish signals during press conferences, hoping Powell's word choice validates their positions. This reactive approach guarantees late entries and exits because tone becomes clear only after prices moved. Institutional money follows different logic entirely, positioning based on where intermediate cycles sit relative to projected paths regardless of Powell's statements.

The distinction between noise and signal becomes clear when examining historical Fed meetings within cycle context. Markets have rallied through hawkish Fed speak when intermediate cycles remained bullish, just as they've declined despite dovish tone when cycles rolled over. The policy tone matters for short-term volatility but rarely overrides the cycle direction already established weeks before meetings. This pattern repeats consistently enough that systematic traders stop reacting to tone and focus on cycle structure instead, learning to read these patterns through practical demonstrations like the example webinar that shows exactly how cycle analysis interprets Fed meetings within larger structural context.

How the 30-Trading-Day Fed Cycle Amplifies Existing Market Rhythm

The Federal Reserve operates on a symmetrical 6-week schedule, meeting approximately every 30 trading days to assess economic data. This creates a predictable timing pattern that traders can overlay on price charts. The pattern shows when volatility typically expands around policy announcements. Knowing that window allows systematic positioning ahead of the event rather than reactive trading after headlines move prices.

When longer-term cycles point higher, Fed meetings create brief pauses before trend resumption. When cycles roll over into decline, Fed decisions accelerate downward momentum regardless of rate cuts. The 30-day rhythm amplifies whatever the intermediate cycle already established. Historical examples show this amplification effect clearly, with identical Fed actions producing opposite market reactions depending on the underlying cycle phase at the time of announcement.

Traders who grasp this relationship stop fighting Fed announcements and use them as predictable volatility windows. The systematic approach involves positioning based on cycle direction before the meeting, then managing that position through the volatility using predefined rules. This becomes particularly important when managing leveraged exposure that requires systematic timing to maximize returns while controlling amplified risk through proper entry and exit signals aligned with TQQQ Trading Strategy With Cycle Context.

Reading Time to Market Through Intermediate Cycle Position Not Fed Speculation

Retail traders spend Fed meeting day speculating about whether Powell sounds hawkish or dovish. They trade the announcement itself, buying or selling based on their interpretation of language nuances. This approach fails because it confuses short-term noise with actual directional signals. Institutional desks ignore the speculation game entirely, focusing instead on where intermediate cycles sit relative to their projected paths.

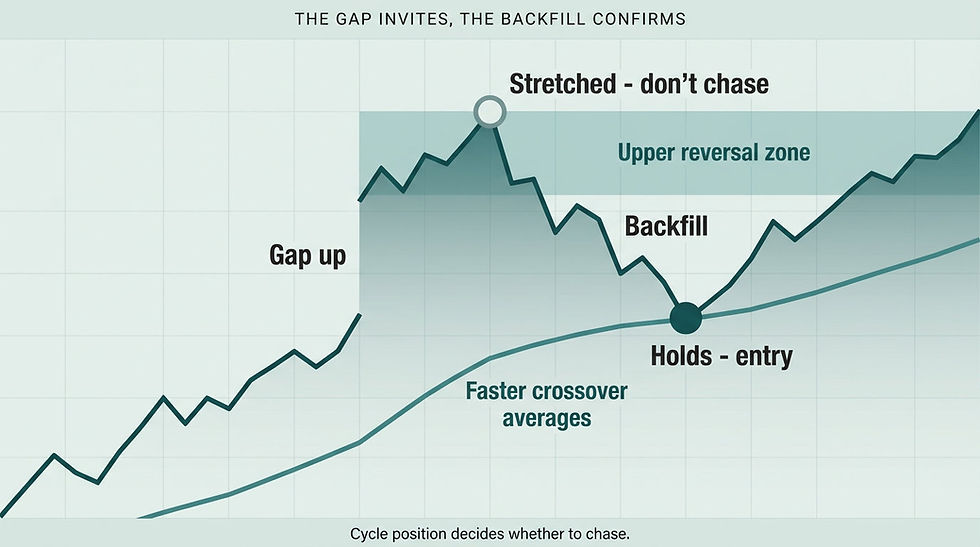

The current intermediate cycle projects strength into mid-November based on the rhythm established over preceding months. Short-term momentum cooled slightly near upper reversal zones, which represents typical behavior before major announcements. Once the Fed statement hits and Powell speaks, volatility expands exactly as the 30-day cycle predicts. But the longer cycle direction remains bullish until structure breaks, meaning any dip tied to hawkish tone creates opportunity rather than signaling trend change.

Institutional money positions for this scenario weeks in advance rather than reacting after the fact. They map probable outcomes based on cycle structure, preparing for both dovish and hawkish scenarios. If cycles project higher and tone comes out dovish, they add to positions. If the same bullish cycle meets hawkish tone creating temporary weakness, they view it as improved entry for the same projected move higher.

Using Crossover Averages to Confirm Time to Market Entries After Fed Volatility

Knowing when cycles project strength provides directional bias, but entry timing requires specific confirmation signals. Crossover averages deliver that validation by measuring whether buying or selling pressure supports the cycle-projected path. The 2/3 and 3/5 crossover averages act as dynamic support levels during uptrends. Stops placed just beneath these averages protect capital if Fed tone shifts hawkish enough to break cycle structure.

A dovish tone today keeps prices moving higher within upper price channels, maintaining alignment with the next cycle crest. If Powell's language turns more restrictive regarding December's meeting, short-term cycles could dip into early November. Either scenario becomes tradable with crossover confirmation because the signals show when to add exposure. The systematic approach removes guessing about Fed tone and replaces it with objective signals based on momentum behavior.

This separation between cycle structure and Fed noise helps traders identify whether volatility represents temporary movement or genuine directional shifts. Short-term spikes driven by forced positioning look different from sustained moves supported by accumulation patterns. Understanding these mechanics allows traders to distinguish between temporary volatility spikes driven by forced positioning versus genuine directional moves supported by accumulation patterns detailed in Short Covering Rally: Understanding the Mechanics and Impact on Market Trends.

People Also Ask About Time to Market

Is now a good time to invest in the stock market?

Time to market depends on cycle position rather than calendar dates or current news sentiment. When intermediate cycles rise and crossover averages confirm upward momentum, systematic entries make sense. The current environment shows intermediate cycles projecting strength into mid-November. This suggests any dips tied to Fed meeting volatility create opportunity rather than signal trend exhaustion.

Retail traders often wait for perfect clarity before positioning, but that clarity arrives only after prices moved higher. Institutional desks position based on probable paths rather than certainty. They use cycle structure to identify when risk-reward favors exposure even if short-term volatility remains elevated. They accept that individual Fed meetings might create temporary pullbacks but maintain positioning as long as intermediate cycles support bullish structure.

Markets reward traders who position ahead of confirmation rather than those who wait for validation. When intermediate cycles rise and crossover averages show intact momentum, the answer becomes yes with proper risk management. That risk management means stops under crossover averages and position sizing appropriate for volatility. The framework works because it defines both entry logic and exit rules before prices force emotional decisions.

How do you know when it's time to get out of the stock market?

Exit timing follows cycle rollover and crossover breakdown rather than reactive selling after headlines create fear. When intermediate cycles peak and begin turning lower, confirmed by crossover average violations, systematic protection makes sense. Until those structural changes appear, short-term volatility around Fed meetings represents normal rhythm. The challenge lies in distinguishing between pullbacks within trends and actual trend changes.

Crossover averages provide that distinction by showing whether dips hold support at key momentum levels. During intact uptrends, prices might touch the 2/3 and 3/5 crossover averages during Fed volatility but bounce quickly. When cycles roll over into decline, prices break beneath crossover averages and fail to reclaim them. That failure confirms the cycle change and validates defensive positioning.

The systematic approach removes guessing about whether current weakness represents buying opportunity or the start of larger decline. Cycles project probable paths weeks in advance, giving traders time to prepare. When intermediate cycles project into mid-November and crossover averages remain intact, the time to exit hasn't arrived. When those cycles peak and momentum indicators confirm the rollover, the exit signal becomes clear without emotion clouding decisions.

What is the 30-day Fed cycle?

The Federal Reserve meets approximately every 30 trading days to assess economic conditions and adjust monetary policy. This creates a symmetrical 6-week timing pattern that repeats throughout the year. The cycle matters for trading because it shows when announcement-driven volatility typically expands. Understanding this rhythm separates positioning ahead of volatility from reactive trading after the fact.

The 30-day Fed cycle doesn't create market direction but amplifies whatever trend the intermediate cycles already established. When longer cycles point higher, Fed meetings create brief pauses and volatility spikes before trend resumption. When cycles roll into decline, Fed announcements accelerate downward momentum regardless of rate cuts. This relationship shows why focusing solely on Fed policy misses the larger structural picture.

Traders who overlay the 30-day Fed cycle on their charts can identify when the next volatility window arrives. This preparation might mean tightening stops before announcements or reducing leverage to manage wider price swings. The systematic use of the Fed cycle transforms announcements from unpredictable events into manageable volatility windows. These windows exist within a larger cycle framework that shows probable direction weeks before Powell speaks.

Do Fed meetings determine market direction?

Fed meetings create short-term volatility but don't establish trend direction over timeframes that matter for positioning. Intermediate and long-term cycles determine whether markets move higher or lower across weeks and months. Fed decisions either accelerate or temporarily pause whatever rhythm those cycles already show. This distinction becomes critical for avoiding the mistake of trading individual announcements as if they override cycle structure.

Historical patterns show that markets climbed walls of worry during Fed tightening cycles when intermediate cycles remained bullish. Markets declined despite Fed easing when cycles rolled over into bear structures. The policy itself mattered less than the timing within the cycle phase. Current Fed communication influences short-term positioning and sentiment, but institutional money follows cycle structure for capital allocation.

The systematic approach recognizes Fed meetings as volatility events within cycle structures rather than determinants of cycle direction. When intermediate cycles rise into mid-November, today's Fed meeting becomes a volatility window for confirming entry signals. That perspective transforms Fed day from stressful speculation into systematic opportunity. The focus shifts from predicting Powell's tone to using announcement volatility for adding exposure when cycle structure aligns favorably.

How do institutions position before Fed announcements?

Institutional money follows cycle structure rather than speculating about Fed tone or trying to predict Powell's language. When intermediate cycles project strength into specific dates weeks ahead, institutions build positioning gradually. They use the 30-day Fed rhythm to anticipate when volatility typically expands. They view that expansion as opportunity for adding exposure if cycles support bullish structure.

The institutional approach involves mapping probable scenarios based on cycle position rather than betting on single outcomes. If intermediate cycles rise and Fed tone comes out dovish, institutions add exposure into the rally. If the same bullish cycle structure meets hawkish Fed tone creating temporary weakness, institutions view the dip as improved entry. This framework works because it separates short-term announcement noise from structural cycle direction.

Retail traders often do the opposite, waiting for Fed meetings to clarify direction before positioning. By the time that clarity arrives, prices already moved significantly and risk-reward turned unfavorable. Institutions accept uncertainty about individual meeting outcomes because cycle structure shows probable direction. This willingness to position ahead of confirmation rather than after everyone else sees signals creates the timing edge.

Resolution to the Problem

The challenge with timing market entries around Fed meetings comes from confusion between short-term noise and structural signals. Every announcement creates volatility that feels significant in the moment. This makes it seem like Powell's tone determines whether markets rise or fall. The perception leads traders to parse every word during press conferences searching for directional clues.

Cycle analysis solves this confusion by showing what drives direction versus what creates temporary price movement. The 30-day Fed rhythm matters because it shows when announcement-driven volatility typically expands. But intermediate cycles determine whether that volatility breaks higher or lower. Separating these layers removes the guessing game about whether to buy or sell based on Powell's language.

The systematic framework replaces reactive speculation with structural positioning based on time patterns that repeat regardless of specific news catalysts. Traders learn to anticipate Fed-driven volatility windows weeks in advance through the 30-day cycle. They then use crossover averages to confirm whether that volatility validates cycle-projected direction or triggers protective stops. Understanding time to market through Fed cycle analysis requires accepting that individual meetings matter less than cycle position, transforming Fed day from stressful speculation into systematic opportunity.

Join Market Turning Point

Most traders waste energy trying to decode Powell's language during Fed meetings, searching for clues about what comes next. They miss the structural rhythm playing out over weeks and months that actually determines direction. The intermediate cycle doesn't care whether Powell sounds dovish or hawkish today because it already established the probable path weeks ago. Understanding this distinction transforms Fed meetings from stressful speculation into systematic opportunities for confirming what cycles already project.

The methodology teaches traders how to read cycle structure that reveals time-based positioning windows before announcements create volatility. You'll learn which crossover signals confirm entries when Fed-driven volatility aligns with cycle direction. The framework removes emotion from timing decisions by defining exactly where structure remains intact and where it breaks down requiring protection. This systematic process aligns your positioning with the same structural patterns institutions follow rather than fighting them through reactive headline trading.

Stop reacting to Fed headlines and start positioning with the same cycle framework institutions use to time entries before volatility arrives rather than after prices already moved. The comprehensive resources show exactly how to read the 30-day Fed cycle within intermediate trend context, which crossover signals confirm entries when announcement volatility aligns with cycle direction, and where to place stops that protect capital if structure breaks.

Conclusion

Time to market isn't about predicting what Powell says during press conferences or whether December brings another rate cut. It comes from reading cycle structure that shows when institutional money positions ahead of volatility. The 30-trading-day Fed rhythm creates predictable expansion windows approximately every 6 weeks. But intermediate cycles determine whether that volatility breaks higher or lower.

Today's Fed meeting will create short-term price movement regardless of Powell's tone. Traders who understand cycle analysis positioned weeks ago based on intermediate cycle structure projecting strength into mid-November. They view today's volatility as confirmation opportunity rather than directional surprise. This systematic approach uses crossover averages to validate whether announcement-driven volatility aligns with cycle-based positioning or triggers protective stops when structure breaks.

Markets reward systematic positioning based on repeating cycle patterns rather than reactive trading based on announcement interpretation. The 30-day Fed cycle shows when volatility arrives while intermediate cycles show which direction that volatility likely breaks. This creates a complete framework for time to market decisions that works regardless of what Powell says on any individual meeting day. The framework separates traders who react to headlines from those who position ahead of them through structural analysis that guides institutional capital allocation.

Author, Steve Swanson