The Impact of Rising Interest Rates on Long-Term Market Cycles and Policy Risk

- May 13, 2025

- 6 min read

Updated: Nov 20, 2025

Rising interest rates aren’t just a monetary lever—they’re a pressure valve on the entire financial system. When rates increase, they don’t act in isolation. They ripple through government budgets, consumer credit markets, investor sentiment, and long-term capital flows. That ripple becomes a tidal force when debt is large and momentum cycles are fragile.

Today, the U.S. faces a clear structural challenge: its national debt has soared past $36 trillion, and interest payments are projected to exceed $1.2 trillion annually. That means the cost of debt service is approaching the size of critical programs like Social Security. And as older, cheaper debt rolls off, it’s being replaced with new debt at higher yields. The impact? A direct compression of fiscal flexibility and a rising drag on economic growth.

For investors tracking long-term cycles, these rate pressures are not short-term headwinds—they are macro-structural pivot points. They influence capital allocation decisions, corporate earnings, housing activity, and even geopolitical risk over extended time-frames.

Rate Hikes Are Fueling a Fiscal Shift

In a low-rate environment, governments can borrow freely without immediate penalty. But as rates climb, the rules change. The U.S. Treasury paid $684 billion in interest during the first half of the fiscal year. At current trends, this could rise to over $1.21 trillion annually—even without further hikes.

Now consider this: if rates increase to 4.5% or 5.0%, interest payments could balloon to $1.63 trillion or even $1.81 trillion per year. That’s not just a higher number—it’s a structural constraint. The federal government will have less room to maneuver on infrastructure, defense, or even recession response. Every dollar spent on interest is a dollar not spent elsewhere.

This fiscal compression forces policy decisions that ripple into markets. Will taxes rise? Will benefits be reduced? Will growth initiatives be put on hold? The answers depend not just on ideology, but on the math of rising interest burdens.

Why Long-Term Market Cycles Are Vulnerable

Interest rates act like gravity on valuations. The higher they go, the more they pull down price-to-earnings multiples, especially for growth stocks that rely on future earnings. But beyond that mechanical relationship, there’s a deeper cycle at work.

When interest payments eat up government budgets, stimulus becomes harder to deliver. Liquidity dries up faster in downturns. Bond issuance surges to fund shortfalls, putting further upward pressure on yields. This feedback loop tightens the system, accelerating the decline of economic and market cycles that were once resilient.

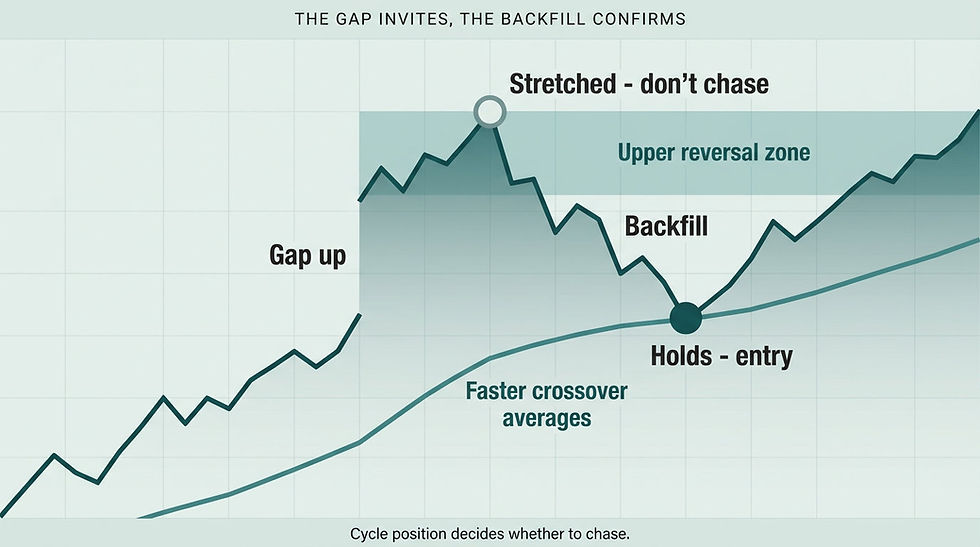

Market Turning Points emphasizes watching price channels, crossovers, and longer-term rhythm shifts. Right now, many of those signals still show an advancing trend—but that doesn’t mean smooth sailing. When cycles peak, and liquidity is constrained, the drop can be faster and deeper than expected. Understanding interest rates within that timing framework becomes critical.

Inflation and Policy Risk Tied to Interest Rate Pressures

Another overlooked risk is how tariffs, taxes, and other policy tools become inflationary when paired with rising rates. Case in point: the U.S. just saw a record $16.3 billion in tariff revenue in April alone. That’s an 86% jump from March. These tariffs act as consumption taxes, raising prices on imported goods. While they boost short-term revenue, they also inject latent inflation into the system.

The Federal Reserve, meanwhile, remains cautious. With CPI numbers only slightly improving, they’ve shown little urgency to cut. If tariffs continue to pressure prices, the Fed may be forced to hold rates higher for longer. That puts added strain on both public finances and interest-sensitive sectors like housing, credit, and tech.

In Steve's cycle philosophy, this becomes a policy risk overlay. Policymakers may unintentionally extend the tightening cycle, worsening the amplitude of the next downturn. As we've seen before, fiscal and monetary errors compound quickly at cycle tops.

Where the Market Stands Right Now

Despite the risks, the market is still pushing upward, driven by momentum cycles and intermediate strength. According to our Visualizer charts, we’re approaching a projected peak between the 14th and 22nd of this month. Momentum is in the upper reversal zone, and short-term cycles suggest a possible pullback to the 5-day moving average in coming sessions.

This doesn’t negate the bullish stance—it sharpens it. Bullish trends don’t last forever, and the healthiest advances respect timing discipline. A pullback now could offer renewed entry points—but we don’t want to be caught unaware when the longer-term cycle finally bends.

Make sure longer positions are protected. Stops below the 4/7 crossover or lower, depending on your time-frame, are essential tools in a rising rate environment. As always, we focus on timing the turns, not chasing the noise.

Also, if you’re navigating ETF trades in this cycle context, check our post on Swing Trading ETFs with Cycle Timing: How to Avoid Late Entries Near Market Tops for more info.

People Also Ask About the Impact of Rising Interest Rates

How do rising interest rates affect the stock market?

Rising interest rates increase the cost of borrowing for companies and consumers alike. For businesses, this means higher expenses to finance growth, which can lead to lower earnings. Investors typically value companies based on future profits, so if those profits are expected to decrease, stock prices often decline. In addition, bonds become more attractive when yields rise, leading many investors to shift capital away from stocks. The result is downward pressure on equity markets, especially in sectors like tech that are more sensitive to capital costs.

Why does the government pay more when interest rates rise?

The U.S. government finances its operations by issuing debt in the form of Treasury bonds. When those bonds mature, the Treasury must issue new bonds at prevailing interest rates. If rates are higher, the new debt comes with higher interest payments. Over time, as more of the national debt is rolled over into higher-rate instruments, the total interest cost increases significantly. With a national debt over $36 trillion, even a modest rise in average rates leads to hundreds of billions more in annual debt service.

Can higher interest rates cause a recession?

Yes, and historically they often have. Higher interest rates slow the economy by making it more expensive for consumers to borrow money (e.g., credit cards, car loans, mortgages) and for businesses to finance operations or expansion. As spending slows, corporate revenues decline, hiring may stagnate or reverse, and economic activity contracts. If this slowdown persists across sectors and job markets weaken, it can trigger a full-blown recession. Central banks walk a tightrope when raising rates—they aim to slow inflation without tipping the economy into contraction.

What happens to housing and real estate when interest rates go up?

Higher interest rates lead directly to higher mortgage rates, making monthly payments more expensive for homebuyers. This reduces home affordability, especially for first-time buyers. As demand weakens, home price growth often slows or reverses. In some markets, prices may fall outright. On the supply side, homeowners with low-rate mortgages become less likely to sell, reducing available inventory. The result is a cooling of both the new construction market and existing home sales, often slowing down real estate transactions across the board.

How do tariffs influence interest rate decisions?

Tariffs raise the cost of imported goods, which feeds into higher overall price levels. This inflationary pressure can influence central banks to delay interest rate cuts or even raise rates to prevent the economy from overheating. If inflation runs hotter than expected because of new tariffs, the Fed may feel compelled to stay restrictive for longer, even if other parts of the economy are slowing. In this way, tariffs indirectly shape monetary policy decisions by altering the inflation landscape.

Resolution to the Problem

The core problem isn’t just high rates—it’s the combination of rising rates, growing debt, and policy responses that lack cycle awareness. Without a focus on timing and structural pressures, investors risk being caught on the wrong side of both economic and market peaks.

By tracking crossover averages and price channels—not just headlines—we gain the tools to anticipate those turning points. Understanding how interest rates shape fiscal constraints, inflation, and cycle dynamics lets us plan proactively rather than react emotionally.

Join Market Turning Points

Want to know when the cycle turns before it shows up in the headlines?

At Market Turning Points, we equip members with daily forecasts, Visualizer charts, and long-term cycle alerts to help you anticipate the market’s real direction. No guessing. No indicators cluttering your screen. Just clear timing and clean structure.

Join us inside and see the difference for yourself.

Conclusion

The impact of rising interest rates is more than a technical adjustment—it’s a trigger point in the long-term structure of markets and policy. As debt costs rise and inflation pressures linger, cycles are becoming more fragile and reactive.

But with the right tools, awareness, and discipline, these risks can be anticipated—not feared. Stay bullish while the trend supports it, but don’t lose sight of the bigger cycle. Rising rates are already shaping the future of capital flows, government budgets, and the next major turning point.

Author, Steve Swanson