Market Rate Meaning: How Interest Rates Shape Economic Cycles and Market Behavior

- Aug 19, 2025

- 8 min read

Why the Market is Obsessed with Rate Cuts?

The current fixation on rate cuts comes from the highly unusual path we've been living through. After the 2008 financial crisis, rates hovered near zero for more than a decade. A decade! That era set expectations for cheap money so high that businesses and households began to treat it as the new normal.

But the dream ended with the sharpest rate-hiking cycle in modern history during 2022-2023, when the Fed lifted rates by more than 500 basis points in less than two years as inflation soared.

Mortgage rates jumped from 2.65% in January 2021 to over 7% by October 2022 as inflation surged to a forty-year peak of 9.1% in June 2022. On a $400,000 loan, the difference was about $1,200 more in monthly payments.

Credit card rates climbed into the mid-20% range, and small-business loans more than doubled in cost. Consumers and companies are still carrying that weight. That's why the market now cheers at the prospect of relief - because even a small cut would feel like some needed oxygen after several years of financial tightening.

A small drop would actually make a big difference. In mid-August 2025, the 30-year mortgage rate slipped to 6.58%, the lowest in nearly a year, and refinancing activity shot up 23%. Cheaper mortgages put buyers back into the housing market. Businesses would use cheaper credit to expand or hire. Our own government could also get relief. For the U.S., even a 0.25% drop could save about $70 billion a year in interest on its $28 trillion of debt.

But that savings doesn't hit at once. Treasuries have about a six-year average maturity - and the reduction would phase in over time as old debt is retired. But it's real money, and it matters. Stocks often respond positively too. Since 1980, the S&P 500 has averaged a 14.1% gain in the twelve months following the first Fed cut of a cycle. Understanding these market dynamics becomes particularly important for swing trading, where cycles and crossovers serve as better guides than rate speculation for beginners.

The flip side is that cuts don't come without risk. They usually happen because growth is slowing or trouble is brewing. Cut too fast and inflation can reignite. Savers get punished as deposit rates fall. Investors, starved for yield, start to push into riskier assets and inflate bubbles.

We've seen that movie before. The housing bubble in the 2000s is a case in point. Mortgage rates had been 8–10% through most of the 1990s, and as high as 18% back in 1981. Then, between 2000 and 2003, they collapsed from about 8% to 5%. That flood of cheaper credit fueled a pent-up wave of homebuying, refinancing, and speculation. It led to lending standards breaking down, and once rates started to climb back, the housing bubble burst, and the fallout became historic.

That's why the current environment stands out. Many are calling for cuts even though employment remains steady and growth hasn't collapsed. As we've studied before, cuts usually line up with recessions.

In 2001, the first emergency cut saw the S&P 500 down 2.5% a week later. In 2007, the first cut gave the market a quick bounce but no staying power as the housing crisis deepened. These examples illustrate why cycle timing and structure matter more than headlines when analyzing market reactions to rate changes.

Compare that to the "insurance" cuts of 1995-96 and 2019, when growth was steady and markets managed solid rallies. Across nine easing cycles since 1974, the S&P has averaged a 30.3% gain, but most of that came only after some deep sell-offs along the way.

That's why all eyes are on Jackson Hole this week. Powell's speech on Friday is being billed as a defining moment. Markets are clammering for clarity: will the Fed hint at a September cut, or will Powell hold the line and risk disappointing traders? We'll soon find out. I'm expecting to hear a more dovish tone.

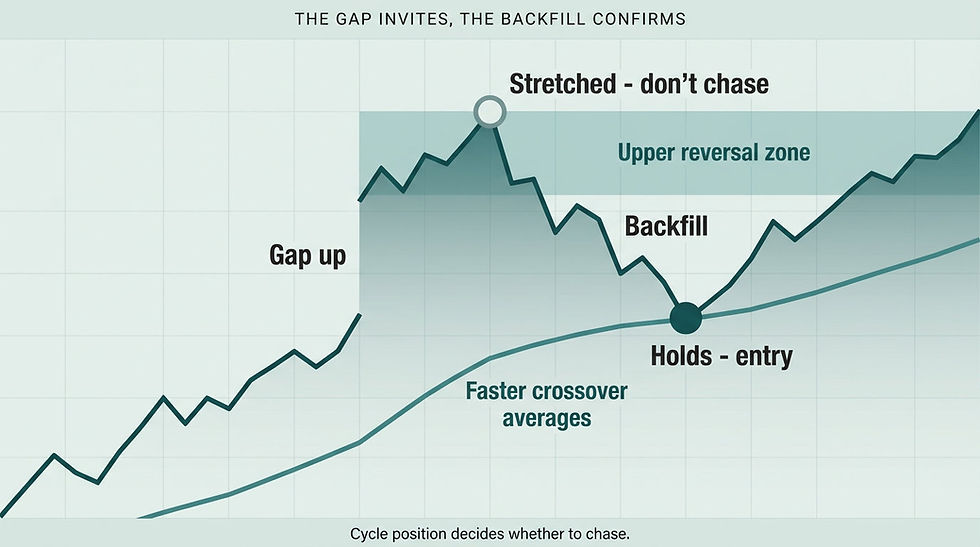

Cycles show weakness into early September, followed by a rally, and then another dip. And should the long-term cycle stay in the upper reversal zone during this time (expected), intermediate dips will continue to be buyable into October. For traders looking to capitalize on these cycle-based opportunities, understanding QQQ strategy approaches that work through crossovers, price channels and cycle timing becomes particularly valuable.

People Also Ask About Market Rate Meaning

What does market rate mean in economics and finance?

Market rate meaning in economics refers to the interest rate determined by supply and demand forces in financial markets, representing the cost of borrowing money or the return on lending capital. This rate reflects the collective assessment of risk, inflation expectations, economic growth prospects, and central bank policy by millions of market participants. Unlike administered rates set by government decree, market rates fluctuate continuously based on changing economic conditions and investor sentiment.

The market rate serves as a crucial price signal that allocates capital throughout the economy, influencing everything from mortgage costs to business investment decisions. When market rates rise, borrowing becomes more expensive, which typically slows economic activity and reduces inflation pressure. When rates fall, cheaper credit stimulates borrowing, spending, and investment, generally accelerating economic growth. Understanding market rate meaning is essential because these rates directly impact personal finances, business operations, and investment returns across all asset classes.

How do market interest rates affect economic cycles?

Market interest rates act as the primary mechanism through which monetary policy influences economic cycles, creating predictable patterns of expansion and contraction. During economic expansion phases, rising demand for credit typically pushes market rates higher, which eventually slows growth by making borrowing more expensive. Conversely, during recessions, falling demand for credit and Fed intervention typically drive rates lower, stimulating economic recovery through cheaper financing costs.

The relationship between market rates and economic cycles creates self-reinforcing feedback loops that amplify both growth and contraction phases. Low rates encourage risk-taking, asset price inflation, and debt accumulation during expansion periods, while high rates force deleveraging, reduce investment, and deflate asset bubbles during contraction phases. This cyclical nature explains why understanding market rate meaning helps predict economic turning points, as rate changes often precede major shifts in economic activity by 6-18 months.

Why do stock markets react strongly to interest rate changes?

Stock markets react strongly to interest rate changes because rates affect multiple fundamental drivers of equity valuations simultaneously. Lower rates reduce the discount rate used in present value calculations, making future corporate earnings more valuable in today's terms and justifying higher stock prices. Additionally, lower rates make dividend-paying stocks more attractive relative to bonds, creating additional demand for equities from income-seeking investors.

The market rate meaning for stocks extends beyond valuation models to include real economic effects on corporate profitability. Lower rates reduce borrowing costs for companies, improving profit margins and enabling expansion investments that drive future earnings growth. They also stimulate consumer spending through cheaper mortgages and credit, increasing revenue for many businesses. Conversely, rising rates create headwinds for both valuations and business fundamentals, explaining why rate changes often trigger significant market movements that persist for months or years.

What's the difference between market rates and Fed rates?

Market rates are determined by supply and demand in financial markets, while Fed rates are policy tools set by the Federal Reserve to influence economic conditions. The Fed sets the federal funds rate, which is the overnight lending rate between banks, but this directly influences only very short-term market rates. Longer-term market rates like mortgages and corporate bonds are determined by market forces, though they're influenced by Fed policy expectations and economic outlook.

The market rate meaning becomes complex because while the Fed can control short-term rates directly, longer-term market rates often move independently based on inflation expectations, economic growth prospects, and global capital flows. This explains why the Fed might cut short-term rates while long-term mortgage rates continue rising, or why market rates sometimes rise in anticipation of future Fed policy changes. Understanding this distinction is crucial because market rates, not Fed rates, determine most borrowing costs that affect economic activity.

How do market rates impact different sectors of the economy?

Market rates impact different economic sectors through varying mechanisms and timelines, creating rotation opportunities as rate cycles evolve. Interest-sensitive sectors like real estate, utilities, and financial services show immediate responses to rate changes, while consumer discretionary and technology sectors experience delayed effects through changed borrowing costs and consumer spending patterns. Banking sectors often benefit from rising rates through improved net interest margins, while real estate and utilities typically suffer from higher financing costs.

The market rate meaning for sector rotation strategies involves understanding these differential impacts and timing sector exposure accordingly. During rate cutting cycles, growth sectors and real estate typically outperform as lower financing costs boost valuations and activity levels. During rate hiking cycles, financial sectors and consumer staples often show relative strength as they benefit from higher rates or maintain pricing power despite economic slowing. This sector rotation pattern creates predictable investment opportunities for those who understand how market rates affect different areas of the economy.

Resolution to the Problem

The fundamental problem with understanding market rate meaning is focusing on Fed policy announcements rather than recognizing how rate changes ripple through economic cycles and market behavior over time. Traders get caught up in predicting whether the Fed will cut 25 or 50 basis points while missing the broader implications of how rate changes affect business investment, consumer behavior, and asset valuations across multiple time horizons.

The solution lies in understanding that market rate meaning encompasses the entire economic transmission mechanism, not just immediate market reactions to Fed communications. Rate changes influence economic cycles through credit availability, investment incentives, and risk-taking behavior that unfold over months and years. This longer-term perspective provides better guidance for positioning than trying to trade Fed meeting outcomes.

Stop focusing on predicting Fed policy and start understanding how rate changes create cyclical opportunities and risks across different economic sectors and time frames. Use the historical patterns we've discussed - rate cuts during recessions versus insurance cuts, sector rotation during rate cycles, and the relationship between credit costs and economic activity - to position for the broader economic implications rather than short-term policy reactions.

Join Market Turning Points

Ready to stop getting whipsawed by Fed rate speculation and start understanding how market rate meaning creates cyclical investment opportunities? Join the Market Turning Points community where we teach you exactly how to analyze interest rate cycles and their impact on different economic sectors and market timing strategies.

You'll learn to recognize how rate changes influence economic cycles, understand the difference between Fed policy and market rate behavior, and most importantly, how to position for sector rotation and market opportunities that develop during different phases of rate cycles. No more guessing what the Fed will do or missing the bigger economic implications.

Join the Market Turning Points community today and discover why understanding market rate meaning provides better investment guidance than Fed policy speculation every time.

Conclusion

Market rate meaning extends far beyond Fed policy announcements to encompass the fundamental mechanisms that drive economic cycles and market behavior. The current obsession with rate cuts reflects the unusual path from zero rates to restrictive policy, creating widespread anticipation for relief that may or may not materialize as expected. Understanding this context helps explain market psychology while revealing the longer-term implications of rate changes.

The historical evidence shows that rate cuts create both opportunities and risks depending on economic context - insurance cuts during stable growth versus emergency cuts during recessions produce very different market outcomes. The key insight is that market rate meaning involves understanding these cyclical patterns and positioning for their economic implications rather than trying to predict exact Fed policy timing.

The next time markets fixate on potential rate cuts, focus on the broader economic cycle context and sector implications rather than Fed meeting speculation. Rates shape economic behavior through credit availability, investment incentives, and risk preferences that create predictable opportunities for those who understand the full meaning of market rate changes rather than just their immediate price effects.

Author, Steve Swanson