4 Percent Rule for Retirement Shows Why Traditional Savings Fall Short and Cycle Timing Offers Alternative Path

- Oct 2, 2025

- 13 min read

The question keeps millions of Americans awake at night: how much money do I really need to retire comfortably? Financial planners have long relied on the 4 percent rule for retirement to frame the answer. According to this guideline, retirees can safely withdraw about 4% of their nest egg each year without running out of money over a 30-year retirement.

The math behind this rule reveals a sobering reality. If you want $60,000 of annual income, you need roughly $1.5 million saved. For a $100,000 per year lifestyle, that number climbs to $2.5 million. With $500,000 saved, a 4% withdrawal provides only about $20,000 a year - barely enough to cover basic expenses. Even at $1 million, the withdrawal comes to just $40,000 annually, and that calculation doesn't account for inflation, healthcare costs, or unexpected emergencies.

These numbers explain why so many people keep working longer than they planned. Traditional buy-and-hold investing strategies can eventually grow accounts into the millions, but that path requires decades of patience and living through deep bear market drawdowns that punish anyone who happens to be retiring at the wrong time.

This is where cycle-based market timing can change the picture. Instead of riding through every downturn like a buy-and-hold investor, our system times market cycles - stepping aside when prices are falling and pressing harder when conditions are favorable. The result is a compounding effect that can dramatically outpace simple buy and hold, though it requires accepting higher risk and active management.

Why the 4 Percent Rule for Retirement Creates a Savings Gap

The 4 percent withdrawal guideline emerged from historical stock and bond market data analyzed by financial planner William Bengen in the 1990s. It assumes a balanced portfolio split between stocks and bonds, consistent annual withdrawals adjusted for inflation, and a retirement lasting 30 years. While the rule provides a starting framework for retirement planning, it comes with significant limitations that many retirees discover too late.

Market conditions matter enormously when applying this rule. The 4% guideline assumes average market performance over your retirement years. If you retire at the beginning of a prolonged bear market, your portfolio may never recover enough to sustain withdrawals. This happened to many who retired in 2000 or 2007, just before major market crashes that devastated their carefully laid plans.

Most importantly, the traditional approach keeps your money fully invested through every market cycle. You ride out the crashes along with the rallies. For someone depending on that portfolio for income, watching your savings drop 30% or 40% during a downturn creates both financial stress and forced selling at the worst possible times. When you're withdrawing money for living expenses during a bear market, you're selling shares at depressed prices that never participate in the eventual recovery. Understanding the difference between strategy structure and execution speed becomes important when comparing various active trading approaches. For traders interested in how cycle timing differs from other methodologies, examining Swing Trading vs Day Trading: Why Structure Beats Speed Every Time provides useful context on why our approach prioritizes market structure over rapid-fire trades.

How Traditional Investing Approaches Fall Short

Buy-and-hold investing has long been positioned as the safe, reliable path to retirement security. The strategy is simple: invest regularly in a diversified portfolio, and wait decades for compound growth to work its magic. For many investors who start early and contribute consistently, this approach does eventually build wealth - but it comes with serious drawbacks that become painfully clear when you need to access that money.

The first problem is time. Building a $1.5 million or $2.5 million portfolio through traditional investing typically requires 30 to 40 years of consistent contributions. If you're starting later in life or playing catch-up after financial setbacks like job losses or divorce, that timeline doesn't work. You can't create decades that don't exist.

The second issue is volatility and sequence of returns risk. Market crashes happen regularly. Since 2000, we've experienced the dot-com crash, the 2008 financial crisis, the 2020 COVID crash, and multiple corrections. Consider what happened to investors who retired in 2007 with $1 million saved. By March 2009, that portfolio had likely dropped to around $600,000. Even if they followed the 4 percent rule and withdrew only $40,000 that first year, they were forced to sell shares at depressed prices. When the market eventually recovered, they owned fewer shares to participate in the rebound, and their portfolio never fully caught up.

Understanding Cycle-Based Market Timing

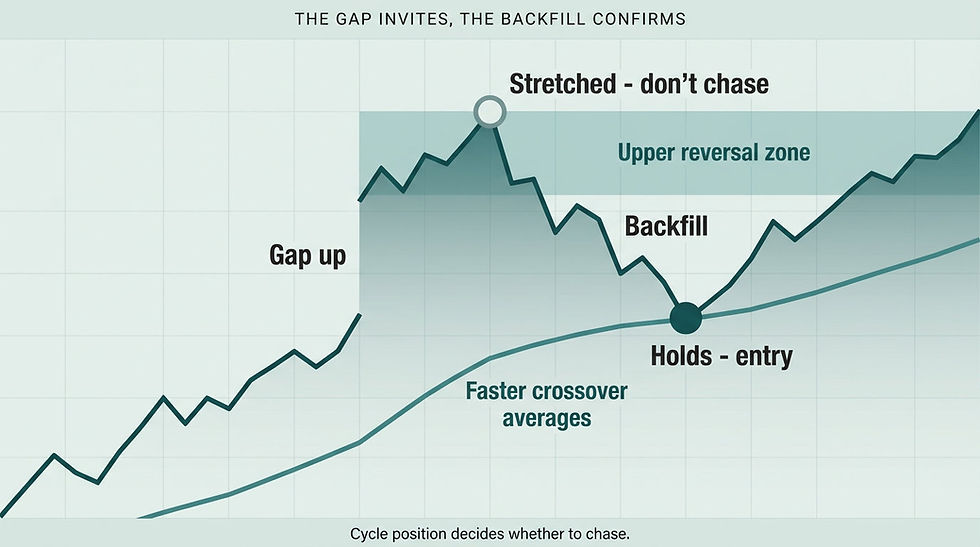

Market cycles represent the natural rhythm of expansion and contraction that occurs across all time frames. Rather than trying to predict specific price levels or guess at news events, cycle timing focuses on identifying where the market sits within its current phase and adjusting position accordingly. This approach recognizes that markets move in waves, not straight lines, and those waves follow identifiable patterns.

This approach uses three core tools: cycle analysis to identify trend direction, price channels to define support and resistance zones, and crossover averages to confirm changes in momentum. These elements work together to provide structure around when to increase exposure and when to step back to cash. None of these tools predict the future - they simply help you recognize current market structure and position accordingly.

The key difference from buy-and-hold is flexibility. When market structure breaks down - when prices fall below established support levels and moving averages cross into bearish configurations - the system signals a move to cash. During favorable market phases, cycle timing often uses leveraged ETFs to amplify returns. For example, SPXL provides 3x daily exposure to the S&P 500. When market structure supports an uptrend and cycles align positively, this leverage can significantly accelerate account growth. When conditions deteriorate, the system moves entirely to cash. For traders who want to explore leveraged strategies specifically, understanding how cycle timing applies to different instruments becomes important. The mechanics of trading inverse and leveraged positions require specific knowledge. Resources like TQQQ and SQQQ Trading Strategy: Outperforming Buy and Hold with Cycle Timing explain how timing signals work across both long and inverse leveraged ETFs, providing insight into the tactical flexibility that makes this approach different from traditional buy-and-hold.

The Reality of Leveraged Trading and Risk

Leveraged ETFs are designed for short-term tactical use, not long-term buy-and-hold positions. In volatile or sideways markets, leveraged ETFs can lose value even when the underlying index remains relatively flat due to daily rebalancing effects. The decay from volatility can erode capital quickly if you're not actively managing positions. This is a fundamental characteristic of how these instruments work, and it cannot be ignored.

The results from our Cycle Signals system demonstrate the potential of this approach, but they also highlight the risks that must be understood. Since 2015, the SPXL Cycle Signal has averaged approximately 83% annual returns in backtesting. Those are exceptional results that dramatically outpace traditional buy-and-hold performance of around 39% annually for the same leveraged ETF. However, it's essential to understand these numbers represent historical backtesting, not live trading results, and they occurred during a predominantly bullish decade for U.S. stocks.

Future market conditions may not resemble the past decade. We could face extended periods of sideways price action, increased volatility, or structural bear markets that challenge even well-designed timing systems. Leverage amplifies both gains and losses, and there will be losing trades and difficult stretches. No system wins every trade, and drawdowns are an inevitable part of active trading. Backtesting applies our signals to historical price data, but backtested results always look better than live trading due to execution slippage, emotional decision-making, and the psychological pressure of real money at risk.

Comparing Returns: What the Numbers Really Mean

The difference between traditional buy-and-hold investing and cycle-based timing becomes clear when you examine long-term compounding effects. Starting with a $25,000 account, traditional buy-and-hold investing in SPXL has produced approximately 39% average annual returns since 2015. Over 10 years, that initial $25,000 would have grown to around $681,000. However, that journey included severe drawdowns. SPXL holders experienced multiple declines of 50% or more during corrections and bear markets. In March 2020, the position dropped roughly 75% in just a few weeks.

By comparison, our Cycle Signals approach for SPXL has averaged approximately 83% annually over the same period in backtesting. At that rate of return, the same $25,000 initial investment would have grown to about $45,688 after one year, crossed $500,000 by year five, and compounded to more than $10 million within 10 years. The weekly average return of 1.14%, monthly average of 4.88%, and annual average of 82.75% represent what the system has achieved historically as calculated daily on our website.

These numbers sound extraordinary because they are. They represent the upper end of what's possible with leverage, favorable market conditions, and effective timing. For someone approaching retirement with limited time to rebuild after losses, these risks matter enormously. The potential for accelerated growth must be balanced against the real possibility of significant drawdowns. A 30% or 40% loss in a retirement account when you're five years from leaving the workforce can be devastating. Past performance does not guarantee future results, and a more prudent expectation might be 30-40% annually - still well above buy-and-hold averages but more sustainable over different market conditions.

Creating Income from Monthly Returns

One of the most compelling aspects of cycle-based timing is the potential to generate regular income from trading returns rather than drawing down principal. This represents a fundamental shift in how retirement income works compared to the traditional 4 percent withdrawal model. Under the 4 percent rule, you're methodically spending down your nest egg each year, hoping it lasts 30 years. The anxiety comes from knowing that every withdrawal reduces the base that generates future returns.

With a well-performing timing system, the goal changes entirely. Instead of depleting principal, you aim to live on the profits generated each month from successful trades. If the system produces consistent positive returns over time, those gains can fund living expenses while leaving the principal intact - or even growing. Consider the hypothetical scenario based on our historical averages: starting with $25,000, the Cycle Signals system's historical performance would compound that into approximately $500,000 within five years. At that account level, the historical monthly average return of 4.88% translates to roughly $24,400 per month.

However, trading returns are not like salary checks - they vary dramatically from month to month. Some months might produce 10% or more, while others could be flat or negative. The 4.88% monthly average includes both winning and losing months spread across a decade. In real-world trading, you'd experience extended stretches where the system underperforms, produces losses, or generates minimal gains. If you're withdrawing money for living expenses, you need substantial buffer capital to cover months when returns disappoint. Tax considerations also significantly affect this approach, as trading profits typically generate short-term capital gains taxed as ordinary income at rates ranging from 22% to 37%. Learning from actual trade examples can provide valuable context for how cycle timing works in practice. For those interested in seeing how our methods apply to real market conditions, reviewing Swing Trading Examples Using Cycle Timing and Price Structure offers concrete illustrations of how we identify entries and exits based on market cycles rather than prediction or guesswork.

Risk Management Requirements

Any serious discussion of leveraged trading and cycle timing must emphasize risk management and realistic expectations. The potential for accelerated returns comes with equally accelerated risk. Without proper risk controls, leverage can destroy trading accounts quickly - sometimes in just a few bad trades. The first principle of sound risk management is position sizing. Professional traders never risk more than 1-2% of their total account value on any single trade.

Stop losses are non-negotiable in this approach. Every trade needs a predefined exit point where you'll cut losses if the position moves against you. Hope is not a strategy, and holding and praying through losing trades is how accounts get destroyed - especially with leverage. When a trade goes bad, you must exit at your planned level and move on to the next opportunity without emotional attachment to being "right."

Even the best trading systems experience losing streaks and drawdowns. You might face extended periods where you give back several months of gains. This is why you should never trade with money you cannot afford to lose. If you're depending on a trading account for immediate living expenses with no other income sources, the stress of drawdowns becomes unbearable. Leverage means you'll experience volatility that feels extreme compared to traditional investing. A 5% move in the S&P 500 translates to a 15% swing in SPXL. Your account balance will fluctuate dramatically day to day. If watching those swings causes stress or anxiety, leveraged trading is not appropriate for you regardless of the potential returns.

What People Also Ask About 4 Percent Rule for Retirement

What is the 4 percent rule for retirement?

The 4 percent rule suggests retirees can safely withdraw 4% of their initial retirement savings annually, adjusted for inflation each subsequent year, without running out of money over a 30-year retirement period. This guideline emerged from research by financial planner William Bengen in the 1990s, analyzing historical stock and bond market data. For example, with $1 million saved, you could withdraw $40,000 the first year, then adjust that amount upward for inflation each following year.

The rule assumes a balanced portfolio split between stocks and bonds and consistent market performance over the retirement period. However, the rule faces significant limitations in today's environment, including lower bond yields, higher stock valuations, and increased life expectancies that challenge its underlying assumptions.

How much money do I need to retire using the 4 percent rule?

To determine your retirement savings target using the 4 percent rule, multiply your desired annual income by 25. If you want $50,000 per year in retirement income, you'd need $1.25 million saved. For $80,000 annually, you'd need $2 million. For $100,000 per year, the target becomes $2.5 million.

This calculation assumes you have no other income sources like Social Security benefits or pensions. The rule provides a starting framework for planning discussions, though individual circumstances may require adjustments based on factors like health, longevity expectations, spending patterns, and the specific market conditions during your retirement years.

What are the biggest problems with the 4 percent rule?

The 4 percent rule faces several critical limitations. First, it assumes average market performance throughout retirement, which becomes highly problematic if you retire just before a major market downturn. This sequence of returns risk can permanently damage your portfolio's ability to sustain withdrawals. Second, the rule doesn't account for variable spending patterns - research shows most retirees spend more in early retirement years and less as they age.

Third, the rule was developed using historical data from a period with higher bond yields and lower stock valuations than today's market environment. Finally, it requires staying fully invested through all market conditions, exposing retirees to devastating drawdowns during bear markets when they're simultaneously withdrawing money for living expenses and selling shares at depressed prices.

Can cycle timing improve retirement income compared to the 4 percent rule?

Cycle timing aims to improve retirement outcomes by actively managing market exposure rather than remaining fully invested through all conditions. By moving to cash during unfavorable market phases and using leveraged positions during favorable trends, the approach seeks to generate returns that significantly exceed buy-and-hold results. Our SPXL Cycle Signals have averaged approximately 83% annually in backtesting since 2015, compared to 39% for buy-and-hold of the same leveraged ETF.

However, this method requires accepting substantially higher risk, increased volatility, active daily management, and the psychological ability to follow signals through losing periods. Leverage amplifies both gains and losses equally. Past results represent backtesting during a favorable market period, and future performance may differ significantly. This approach demands proper risk management, adequate capital buffers, and realistic expectations about variability.

Is the 4 percent rule still valid in 2025?

The 4 percent rule faces increased scrutiny in current market conditions due to changed circumstances compared to when it was developed. Lower bond yields, higher stock valuations, increased life expectancies, and the possibility of extended market downturns all challenge the rule's underlying assumptions. Some financial planners now suggest 3.5% or even 3% as more conservative withdrawal rates given today's market environment.

Additionally, the rule doesn't account for modern realities like rapidly increasing healthcare costs, longer retirements due to increased longevity, and the possibility of multi-year bear markets. While it remains a useful starting point for retirement planning discussions, most experts recommend personalizing withdrawal strategies based on individual circumstances rather than rigidly following any single guideline.

Resolution to the Problem

The fundamental problem with the 4 percent rule for retirement is that it requires enormous capital accumulation - often $1.5 to $2.5 million - that most people cannot realistically save through traditional investing within their working years. For those starting late, recovering from financial setbacks, or simply unable to save aggressively for decades, the math simply doesn't work. You're left working longer than desired or accepting a reduced standard of living in retirement.

Cycle-based market timing offers a potential alternative path by attempting to accelerate wealth accumulation through active management of market exposure. By stepping aside during unfavorable market conditions and using leverage during favorable trends, the approach aims to generate returns that dramatically outpace traditional buy-and-hold strategies. The historical performance of our Cycle Signals system demonstrates what's possible when timing and leverage combine effectively under favorable conditions.

However, this alternative path demands accepting significantly higher risk, dealing with increased volatility, developing the psychological discipline to follow signals through inevitable losing periods, and maintaining realistic expectations about future performance. It requires active daily management, strict risk controls, adequate capital buffers for drawdowns, and the emotional fortitude to handle leverage-induced account swings. For traders with appropriate capital, risk tolerance, and temperament, cycle timing represents a genuine alternative worth considering. For others, particularly those close to retirement with limited capital to risk or uncomfortable with trading volatility, the traditional path remains more appropriate despite its limitations.

Join Market Turning Points

Ready to explore whether cycle-based timing could fit into your retirement planning strategy? Market Turning Points teaches you exactly how to identify market cycles, recognize when trends are pausing versus reversing, and position yourself for the next leg higher. Our systematic approach removes guesswork from timing decisions and provides structure for managing leveraged positions.

You'll learn to read our cycle indicators, understand crossover signals, and use price channels to confirm trend strength. We show you how to manage risk properly through position sizing and stop placement, and more importantly, how to maintain discipline through losing periods when emotions run high. No promises of guaranteed results - just honest education about what works, what doesn't, and why.

Start learning cycle timing strategies with Market Turning Points. Get access to daily cycle analysis, real-time signal updates, and join a community of traders who understand that sometimes the best opportunities come from managing risk as carefully as pursuing returns. Visit the Stock Forecast Today homepage to learn more about our approach to market cycles, timing signals, and alternative strategies for building retirement security.

Conclusion

The 4 percent rule for retirement provides a useful planning framework, but it exposes a harsh reality: most people need far more capital than they'll realistically accumulate through traditional investing. For those with limited time or playing catch-up after financial setbacks, the decades required to reach $1.5 to $2.5 million simply don't exist. This gap between retirement needs and achievable savings drives people to work longer than they'd prefer or accept reduced living standards in their later years.

Cycle-based market timing offers an alternative approach that could potentially accelerate wealth accumulation by actively managing market exposure rather than passively riding through all conditions. The historical results from leveraged timing strategies demonstrate compelling possibilities. However, these results come with substantial caveats about risk, volatility, psychological challenges, and the critical difference between backtested performance and live trading reality.

The choice isn't about which approach is objectively superior - it's about which approach better serves your specific situation, timeline, risk tolerance, and psychological makeup. Traditional buy-and-hold offers simplicity and predictability at the cost of requiring decades and enormous capital. Cycle timing offers potential for accelerated growth at the cost of accepting higher risk and demanding active management. Neither path guarantees success, and both require honest assessment of your circumstances before committing. Understanding your options, their trade-offs, and their limitations is what enables informed decisions rather than gambling on hope.

Author, Steve Swanson