Market Algorithms Show Why Warren Buffett Could Make 50 Percent on Small Accounts Using Systematic Timing

- Sep 29, 2025

- 10 min read

I love this quote from Warren Buffett in a 1999 Businessweek article:

"If I was running $1 million today, or $10 million for that matter, I'd be fully invested. Anyone who says that size does not hurt investment performance is selling. The highest rates of return I've ever achieved were in the 1950s. I killed the Dow. You ought to see the numbers. But I was investing peanuts then. It's a huge structural advantage not to have a lot of money. I think I could make you 50% a year on $1 million. No, I know I could. I guarantee that."

He was right - and our Cycle Signals are proof of it. They routinely exceed that kind of performance every single year. The only difference is we are even less 'passive' and don't stay "fully invested" unless cycles say it's time. We step in when the cycles tell us the market is going to be turning higher, and we step aside when those same cycles show otherwise.

Even Warren didn't stay fully invested ahead of the dot-com crash of 2000 or the banking crisis of 2008. In fact, he was criticized for being too conservative and even out of touch in 1999 Barron's article that asked, "What's Wrong, Warren?"

That's our advantage. We never ride a bear market or correction to its next low. Instead of being permanently invested, our significant edge is our algorithmic timing - knowing when it's time to press forward and when it's time to protect capital. It's the same rhythm institutions are using as they rotate money in and out around economic data, Fed meetings, and earnings seasons.

The difference between a large investment firm and us is simple: we're small, nimble, and free to act without the weight of billions holding us back. That structural advantage is what allows us to keep compounding at a pace Buffett guaranteed he could do - but with a risk profile that's built to take advantage of today's type of more volatile action.

The beauty of our approach is that we can move faster, scale quicker, and capture the kind of gains that compound far beyond what buy-and-hold will ever deliver.

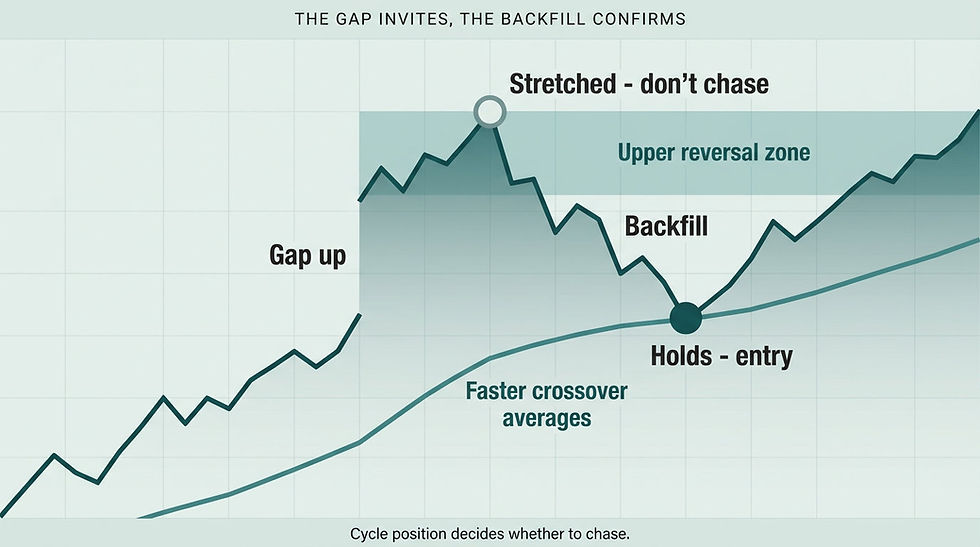

Right now, short-term cycles are bouncing out of the lower reversal zone, but with intermediate cycles weaker and projected cycles showing a dip into the first week of October, this bounce should be treated as temporary. In other words, this isn't likely the start of the next leg higher yet - it's the rhythm of a relief rally inside an intermediate pullback.

Why Small Account Size Creates Warren Buffett's Guaranteed Performance Edge

The structural advantages Buffett referenced in 1999 stem from fundamental market mechanics that large institutions cannot overcome regardless of their analytical capabilities or resources. When managing billions of dollars, position entry and exit activities create price impact that erodes returns before trades complete, while smaller accounts can execute full positions at desired prices without moving markets.

This size advantage extends beyond simple execution mechanics into opportunity selection. Large funds must focus on liquid large-cap securities where they can deploy meaningful capital, eliminating thousands of potential opportunities available to smaller accounts. The mathematical reality is that a $1 million account can fully position in securities that would be meaningless for billion-dollar funds.

Market algorithms amplify these structural advantages by providing systematic timing precision that combines nimbleness with disciplined decision-making. While institutions struggle with position sizing constraints and market impact costs, algorithmic approaches allow small accounts to capture the full performance potential Buffett described. The key lies in understanding that size limitations create opportunity constraints that no amount of research or analysis can overcome for large funds. This systematic approach to identifying when broader market participation weakens becomes particularly valuable for smaller accounts seeking to preserve capital during distribution phases, as detailed in Market Breadth Indicators Reveal Why the Rally May Be Weaker Than It Appears.

How Market Algorithms Deliver the Timing Precision Buffett Couldn't Scale

The performance Buffett achieved in the 1950s relied on intensive research identifying undervalued securities combined with concentrated positioning - a methodology that becomes impossible to maintain at scale. Market algorithms provide a different path to similar returns by focusing on timing precision rather than security selection, creating an approach that works specifically because of small size rather than despite it.

Algorithmic cycle analysis identifies when institutional money flows create conditions for sustained moves higher versus when distribution patterns suggest temporary rallies within corrections. This timing precision allows systematic capture of trend moves while avoiding the drawdown periods that erode buy-and-hold returns. The mathematical advantage comes from being invested only during favorable conditions rather than enduring full market cycles.

Buffett's 1999 comment about guaranteed 50% returns reflected his understanding that small accounts could exploit opportunities unavailable to Berkshire Hathaway. Market algorithms extend this concept by adding systematic timing discipline that removes the emotional decision-making that often causes small investors to underperform despite their structural advantages. The combination of nimbleness and algorithmic precision creates the performance potential Buffett described.

The Institutional Rotation Pattern That Small Accounts Can Exploit

Professional money management operates around systematic calendar events including economic data releases, Fed meetings, and earnings seasons. These institutional rotation patterns create predictable periods when capital flows intensify or diminish, generating opportunities for accounts small enough to position ahead of these moves without creating market impact.

Large funds cannot exploit these patterns effectively because their position sizing requirements force them to build positions over extended periods, eliminating the timing advantages that rotation patterns provide. By the time billion-dollar funds complete position changes, the opportunities that drove their decisions often no longer exist at favorable prices.

Market algorithms track these institutional rotation rhythms through cycle analysis that identifies when multiple factors converge to create high-probability turning points. The systematic nature of this approach removes the subjective interpretation that causes most traders to mistakenly position ahead of or after optimal entry windows. Small accounts gain their edge by matching institutional timing precision without the execution constraints that limit large fund performance.

Why Buffett Avoided Bear Markets Despite Buy and Hold Philosophy

The narrative that Buffett practices pure buy-and-hold investing misses crucial details about how Berkshire Hathaway actually manages capital. His criticism during 1999 for being "out of touch" reflected his unwillingness to participate in technology bubble valuations, while his positioning ahead of 2008 demonstrated similar timing discipline that protected capital during the financial crisis.

This selective participation approach aligns with algorithmic market timing despite differences in implementation methodology. Buffett's value investing framework provided timing discipline through valuation analysis, while market algorithms use cycle patterns and technical structure. Both approaches share the fundamental principle that being invested only during favorable conditions produces superior returns compared to permanent market exposure.

The key distinction is that small accounts can implement this timing discipline more effectively than Berkshire Hathaway because position changes don't create market impact or require extended execution periods. Market algorithms provide the systematic framework for making these timing decisions without the valuation analysis constraints that limit opportunity selection for value investors. Understanding how to identify when temporary weakness within ongoing trends creates optimal entry conditions becomes particularly important for implementing this selective participation approach, as explored in Bullish Continuation Patterns That Align With Intermediate Cycle Timing.

Algorithmic Timing Advantages in Modern Volatile Markets

Today's market environment creates even greater opportunities for algorithmic timing approaches compared to Buffett's 1950s experience. Increased volatility from algorithmic trading, options activity, and social media-driven sentiment swings produce larger intraday and day-to-day price movements that systematic timing can exploit while buy-and-hold investors simply endure.

The mathematical advantage of avoiding drawdown periods compounds dramatically over time. While buy-and-hold approaches eventually recover from corrections, the capital preservation during decline phases allows algorithmic approaches to reinvest at more favorable levels. This compounding effect on reinvestment creates the performance separation that Buffett described as possible for small accounts.

Modern market structure actually enhances these timing advantages because increased volatility creates more distinct cycle patterns and technical levels that algorithmic analysis can identify. The same volatility that frustrates buy-and-hold investors provides the price movement that systematic timing approaches require for optimal performance. Small accounts gain additional advantages by avoiding the behavioral mistakes that cause most investors to sell during corrections and buy during rallies.

Current Cycle Structure Shows Timing Discipline in Practice

The current market environment demonstrates how algorithmic timing discipline operates in practice. Short-term cycles bouncing from lower reversal zones create temporary strength that appears bullish to buy-and-hold investors, but intermediate cycle weakness and projected October dips suggest this represents relief rally conditions rather than sustained advance initiation.

This distinction becomes crucial for capital preservation and optimal positioning. Buy-and-hold approaches must remain invested regardless of intermediate cycle structure, accepting whatever returns the next several weeks deliver. Algorithmic timing allows recognition that current conditions favor caution despite short-term bounce patterns, protecting capital for deployment when cycle alignment improves.

The systematic nature of this analysis removes emotional decision-making that causes most investors to chase temporary strength or panic during weakness. Market algorithms identify these conditions through mathematical cycle relationships rather than subjective interpretation, providing the timing precision that creates performance advantages Buffett described. Applying systematic timing to specific instruments while managing risk through technical levels helps small accounts capture these opportunities effectively, as detailed in QQQ Strategy That Works: Trade the Decline With Crossovers, Price Channels and Cycle Timing.

People Also Ask About Market Algorithms and Small Account Performance

How do market algorithms help small accounts achieve Warren Buffett's guaranteed 50 percent returns?

Market algorithms help small accounts achieve exceptional returns by providing systematic timing precision that exploits the structural advantages Buffett described - nimbleness, minimal market impact, and unlimited opportunity selection. Algorithmic approaches identify optimal entry and exit windows through cycle analysis, allowing small accounts to be invested only during favorable conditions rather than enduring full market cycles that erode buy-and-hold returns.

The combination of small size advantages and algorithmic timing discipline creates conditions where 50% annual returns become mathematically achievable through consistent capture of trend moves while avoiding drawdown periods. Unlike large funds constrained by position sizing and execution challenges, small accounts using market algorithms can fully exploit the performance potential that Buffett guaranteed was possible with proper methodology.

What makes algorithmic timing better than Warren Buffett's value investing approach for small accounts?

Algorithmic timing and value investing represent different methodologies for achieving similar goals - selective market participation during favorable conditions. Value investing relies on fundamental analysis to identify undervalued securities, while algorithmic approaches use cycle patterns and technical structure to optimize entry and exit timing regardless of security selection.

For small accounts, algorithmic timing offers advantages in implementation simplicity and opportunity frequency. Value investing requires intensive fundamental research to identify undervalued situations, while algorithmic approaches provide systematic signals based on mathematical relationships. Additionally, algorithmic timing generates more frequent opportunities because cycle patterns repeat regularly, while compelling value situations may be scarce during certain market environments.

How did Warren Buffett avoid major bear markets if he practices buy and hold investing?

Warren Buffett's actual investment approach includes more timing discipline than pure buy-and-hold philosophy suggests. His technology sector avoidance during the late 1990s and defensive positioning ahead of 2008 demonstrate selective participation based on valuation analysis rather than permanent market exposure regardless of conditions.

This selective approach aligns with algorithmic timing principles despite different implementation methods. Buffett uses fundamental valuation to determine when market prices justify participation, while algorithmic approaches use cycle analysis and technical structure. Both methodologies share the core principle that being invested only during favorable risk-reward conditions produces superior returns compared to permanent market exposure.

Why can't large investment funds replicate Warren Buffett's 1950s performance?

Large investment funds cannot replicate Buffett's 1950s performance because size creates insurmountable structural disadvantages. Position entry and exit activities for billion-dollar funds create market impact that erodes returns, while opportunity selection becomes limited to liquid large-cap securities where meaningful capital deployment is possible.

The mathematical reality is that a fund managing $100 billion cannot exploit the same opportunities available to a $1 million account. Execution constraints, market impact costs, and limited opportunity selection combine to cap potential returns regardless of analytical capabilities or research resources. This explains why Buffett guaranteed 50% returns on small accounts while acknowledging that Berkshire Hathaway's size prevents similar performance.

How do current market algorithms compare to Warren Buffett's 1950s methodology?

Current market algorithms and Buffett's 1950s methodology differ significantly in implementation but share fundamental principles about selective participation and exploiting structural advantages. Buffett used intensive fundamental research to identify undervalued securities, while modern algorithms use cycle analysis and technical patterns to optimize timing.

The key similarity lies in recognizing that superior returns require systematic discipline rather than permanent market exposure. Buffett's concentrated positions in undervalued securities and modern algorithmic timing both exploit conditions that large funds cannot access effectively. Current algorithms benefit from increased market volatility and advanced analytical tools unavailable in the 1950s, while maintaining the nimbleness advantages that Buffett described as crucial for exceptional performance.

Resolution to the Problem

The challenge small investors face lies in recognizing their structural advantages rather than attempting to compete with institutional resources in areas where size creates disadvantages. Warren Buffett's 1999 guarantee about 50% returns on small accounts reflected his understanding that nimbleness and opportunity selection advantages outweigh the analytical resources and research capabilities that large funds possess.

Market algorithms provide the systematic framework for exploiting these structural advantages through timing precision that combines small account nimbleness with disciplined decision-making. The mathematical advantages of avoiding drawdown periods, executing positions without market impact, and accessing unlimited opportunity selection create conditions where exceptional returns become achievable rather than theoretical.

Effective implementation requires embracing algorithmic timing discipline rather than attempting to replicate institutional approaches that work despite size constraints rather than because of them. When small accounts focus on their natural advantages through systematic timing methodologies, they access the performance potential Buffett described as guaranteed with proper approach.

Join Market Turning Points

At Market Turning Points, we teach our community how to exploit the structural advantages Warren Buffett described through market algorithms that provide systematic timing precision. Our approach helps members understand how to leverage nimbleness and opportunity selection flexibility that large funds cannot access regardless of their resources.

Our algorithmic cycle analysis provides the timing framework needed to be invested only during favorable conditions rather than enduring full market cycles. Rather than attempting to compete with institutional research capabilities, members learn to exploit the advantages that come naturally to small accounts through systematic methodologies designed specifically for nimble implementation.

The community focuses on developing the timing discipline that creates performance separation between algorithmic approaches and buy-and-hold strategies. Understanding how to identify optimal entry and exit windows through cycle analysis helps members capture the compounding advantages that Buffett guaranteed were possible for small accounts. Discover how systematic timing exploits structural advantages unavailable to large funds regardless of their analytical resources.

Conclusion

Market algorithms demonstrate why Warren Buffett could guarantee 50% annual returns on small accounts by providing systematic timing precision that exploits structural advantages large funds cannot overcome. The combination of nimbleness, minimal market impact, and unlimited opportunity selection creates conditions where exceptional performance becomes achievable through disciplined implementation rather than remaining theoretical.

The key insight lies in understanding that small size represents a competitive advantage rather than limitation when combined with proper systematic methodology. Algorithmic timing provides the framework for exploiting these advantages through cycle analysis that identifies optimal participation windows, allowing small accounts to avoid the drawdown periods that erode buy-and-hold returns.

Successful implementation requires embracing the selective participation approach that both Buffett's 1950s methodology and modern algorithmic timing share - being invested only during favorable conditions rather than enduring full market cycles. Current cycle structure showing temporary bounce within intermediate weakness demonstrates this timing discipline in practice, protecting capital for deployment when alignment improves rather than accepting whatever returns immediate participation delivers.

Author, Steve Swanson