Long Term Trading When Combined with Institutional Cycle Timing

- Sep 20, 2025

- 13 min read

Long term trading when combined with institutional cycle timing represents the most sophisticated approach to capturing extended market moves that develop over months or quarters, allowing traders to participate in the largest and most predictable institutional money flows. Unlike short-term strategies that attempt to profit from daily volatility or intermediate approaches focused on weeks, long term trading aligns with the fundamental rhythm of institutional portfolio management cycles that drive the most substantial and sustainable market trends. When properly executed using institutional cycle analysis, this approach can capture 20-50% moves over 3-12 month periods while maintaining lower stress and time commitment than shorter time-frame strategies.

The power of combining long term trading with institutional cycle timing lies in understanding how major institutional players manage their portfolios according to quarterly earnings cycles, annual rebalancing periods, and multi-year allocation shifts that create predictable patterns of accumulation and distribution. Professional money managers don't make random decisions but follow systematic approaches based on performance measurement periods, regulatory requirements, and fiduciary responsibilities that create cyclical behavior patterns. By aligning long term trades with these institutional cycles, individual traders can position themselves ahead of major capital flows rather than reacting to price movements after institutional decisions have already been implemented.

Understanding long term trading through institutional cycle analysis requires recognizing that the largest profit opportunities come from identifying when multiple institutional factors converge to create sustained directional pressure over extended periods. When Federal Reserve policy cycles align with corporate earnings growth phases while institutional performance measurement creates favorable allocation environments, the resulting price movements can persist for months or quarters rather than days or weeks. This systematic approach transforms long term trading from hoping for favorable outcomes into positioning ahead of predictable institutional behavior that drives the most significant market movements over extended time-frames.

Institutional Portfolio Cycles and Long-Term Positioning

Effective long term trading requires understanding how institutional portfolio management cycles create predictable windows of opportunity that can be identified and exploited through systematic cycle analysis. Major institutional investors operate according to quarterly performance reviews, annual allocation adjustments, and multi-year strategic planning cycles that create rhythmic patterns of buying and selling pressure throughout different calendar periods. These cycles don't operate randomly but follow established patterns based on performance measurement, regulatory deadlines, and fiduciary responsibilities that create opportunities for individual traders who understand the timing.

The quarterly earnings cycle creates one of the most reliable frameworks for long term institutional positioning because corporate results drive fundamental allocation decisions that institutional money managers must implement over extended periods. When companies demonstrate consistent earnings growth aligned with institutional cycle projections, professional money flows into these positions gradually over months rather than creating immediate price spikes that dissipate quickly. Understanding how earnings cycles interact with institutional allocation timing allows long term traders to position ahead of these sustained buying programs rather than chasing price movements after institutional decisions become obvious.

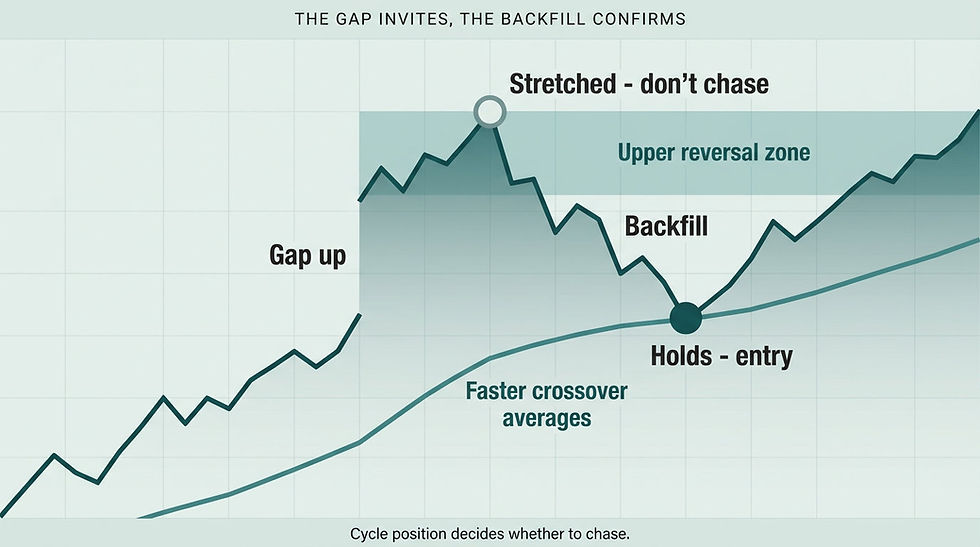

Annual rebalancing cycles provide another systematic framework for long term trading because institutional portfolios must be adjusted according to target allocations that have shifted due to performance variations throughout the year. When certain sectors or asset classes outperform or underperform significantly, institutional managers must systematically buy or sell to restore proper portfolio balance, creating predictable flows that can persist for weeks or months. Long term traders who understand these rebalancing cycles can position ahead of institutional flows rather than competing with them during implementation periods. Check our post on How to Swing Trade Using Cycle Timing and Price Structure, Not Emotion for more info.

Federal Reserve Policy Cycles for Extended Trades

Long term trading success requires integrating Federal Reserve policy cycles with institutional behavior patterns to identify extended periods when policy direction aligns with institutional allocation strategies. Fed policy cycles typically operate over 12-24 month periods, creating sustained environments that favor certain asset classes or market sectors for extended periods rather than temporary shifts that reverse quickly. When Fed policy supports institutional risk-taking through accommodative monetary conditions, long term trades can capture sustained upward momentum that persists until policy cycles shift toward restrictive conditions.

The transition periods between Fed policy phases create particularly important opportunities for long term positioning because institutional managers must adjust their portfolios gradually to accommodate changing interest rate environments and liquidity conditions. When Fed cycles shift from restrictive to accommodative policies, institutional buying programs often develop over months as professional money managers increase risk allocation systematically rather than making immediate dramatic changes. Understanding these transition timing patterns allows long term traders to position ahead of institutional flows rather than reacting after policy changes become fully implemented.

Interest rate cycle analysis provides essential context for long term trading because institutional behavior varies significantly based on the direction and magnitude of rate changes over extended periods. During declining rate environments, institutional money typically flows into growth assets and risk-sensitive sectors that benefit from lower borrowing costs and improved valuation multiples. Conversely, rising rate cycles often favor value sectors and dividend-paying assets that provide income alternatives to bonds while maintaining institutional allocation requirements. Long term traders must understand these cyclical preferences to position appropriately for extended holding periods.

Calendar-Based Institutional Events for Multi-Month Trades

Calendar-based institutional events create systematic opportunities for long term trading because major money management decisions cluster around specific dates that create predictable patterns of institutional behavior over extended periods. Year-end portfolio positioning, quarterly rebalancing periods, and annual strategic allocation reviews all generate institutional flows that develop over weeks or months rather than creating temporary price movements that reverse quickly. Understanding these calendar patterns allows long term traders to position ahead of institutional decisions rather than reacting to price movements after implementation begins.

The December-January institutional cycle provides particularly reliable long term trading opportunities because year-end tax considerations and new-year allocation decisions create sustained institutional flows that often persist through the first quarter. When institutional tax-loss selling creates temporary weakness in December, followed by new allocation money in January, the resulting price movements can create multi-month trends that offer substantial profit opportunities for properly positioned long term trades. Professional traders study these annual patterns to identify sectors or individual positions that benefit from predictable institutional behavior cycles.

Quarterly options expiration and earnings announcement cycles interact with institutional decision-making to create extended trading opportunities that can be quantified and exploited through systematic analysis. When major institutional holdings report earnings during specific calendar windows, the resulting allocation adjustments often develop over several weeks as portfolio managers implement position changes gradually rather than creating dramatic immediate shifts. Long term traders who understand these timing patterns can position ahead of institutional implementation rather than competing with professional money during adjustment periods. Check our post on Swing Trading Indicators: The Only Three That Matter for Timing and Clarity for more info.

Long Term Trading Risk Management for Extended Holding Periods

Long term trading using institutional cycle timing requires sophisticated risk management approaches that account for the extended volatility exposure and capital commitment that multi-month positions create. Unlike short-term strategies where positions can be adjusted quickly, long term trades must withstand normal market fluctuations over extended periods while maintaining systematic criteria for position adjustment or exit. This requires understanding how institutional cycles can experience timing variations or interruptions that might delay expected outcomes without invalidating the underlying institutional thesis.

Position sizing for long term trades must account for the increased capital commitment and psychological stress that extended holding periods create, requiring more conservative allocation than shorter time-frame strategies despite potentially larger profit targets. When positions represent significant portfolio percentages held over months, normal market volatility creates larger emotional stress that can interfere with systematic decision-making during temporary adverse movements that don't invalidate the institutional cycle analysis. Professional long term traders typically use 1-3% position sizes to maintain psychological stability while capturing meaningful profits from successful institutional cycle positioning.

Stop-loss management for long term institutional cycle trades requires understanding the difference between normal cycle timing variations and genuine cycle breakdown that invalidates the original positioning thesis. Institutional cycles can experience delays of several weeks or months due to unexpected events or policy changes that don't necessarily invalidate the longer-term institutional patterns. Long term traders must develop systematic criteria for distinguishing between temporary delays that require patience and fundamental changes that require position adjustment or exit regardless of unrealized loss implications.

Multi Time-frame Cycle Analysis for Long-Term Success

Successful long term trading requires analyzing institutional cycles across multiple time-frames to ensure that shorter-term patterns support rather than conflict with extended holding period strategies. While long term trades focus on quarterly and annual institutional cycles, understanding how monthly and weekly patterns interact with longer cycles helps optimize entry timing and position management throughout extended holding periods. This multi-layered approach ensures that long term positioning aligns with both immediate institutional patterns and extended cycle projections.

The relationship between different cycle time-frames creates optimization opportunities when shorter patterns provide favorable entry points within longer-term institutional trends. When weekly institutional flows align with monthly allocation cycles while quarterly patterns support extended directional bias, long term position timing can be optimized for maximum profit capture while minimizing drawdown exposure during normal volatility periods. However, when time-frames diverge with short-term patterns conflicting with longer cycles, position timing should favor longer-term institutional patterns despite apparent short-term opportunities.

Long-term cycle confirmation becomes essential for position confidence during extended holding periods when temporary adverse movements test trader conviction despite intact institutional analysis. When multiple time-frame cycles align to support directional bias over extended periods, long term traders can maintain position confidence during normal volatility that might otherwise trigger premature exits. Understanding how different cycle lengths interact helps distinguish between temporary technical corrections and genuine institutional pattern changes that require position reassessment. Check our post on Market Breadth Indicators Reveal Why the Rally May Be Weaker Than It Appears for more info.

Profit Optimization Through Extended Institutional Trends

Long term trading profit optimization requires understanding how institutional trends develop over extended periods to maximize position management throughout different phases of institutional cycle development. Early institutional accumulation phases offer the best risk-reward opportunities for long term positioning because professional money flows create sustained momentum with limited downside risk as institutional support builds gradually. However, late-cycle phases require different management approaches as institutional profit-taking begins and momentum shifts toward distribution rather than accumulation.

The scaling approach to long term position management allows traders to optimize profit capture throughout different phases of institutional cycle development rather than maintaining static positions regardless of changing cycle characteristics. During early accumulation phases, positions can be gradually increased as institutional support builds and cycle confirmation strengthens. Conversely, during late accumulation or early distribution phases, partial profit-taking becomes appropriate while maintaining core positions for potential final moves before institutional selling begins.

Extended holding period psychology requires understanding that long term trading profits often develop slowly with extended periods of consolidation followed by rapid acceleration when institutional decisions reach implementation phases. This pattern creates psychological challenges because extended periods without significant progress can create doubt about position validity despite intact institutional cycle analysis. Professional long term traders prepare for these psychological challenges by understanding that institutional cycle timing often experiences delays that don't invalidate the underlying analysis but require patience and systematic position management throughout extended development periods.

People Also Ask About Long Term Trading When Combined with Institutional Cycle Timing

How long should long term trading positions be held?

Long term trading positions should typically be held for 3-12 months depending on how institutional cycle development aligns with the original positioning thesis and whether cycle timing unfolds as projected. The optimal holding period is determined by institutional cycle completion rather than arbitrary time targets, with positions maintained as long as institutional patterns continue supporting the directional bias through accumulation or distribution phases. When institutional cycles complete their projected patterns or shift fundamentally, holding periods should be adjusted regardless of elapsed time since position entry.

Professional long term traders use institutional cycle milestones as dynamic management criteria rather than predetermined time stops, recognizing that institutional accumulation or distribution phases can extend beyond typical quarterly periods when market conditions support sustained directional movement. The key is maintaining positions while institutional patterns support the trade thesis while remaining flexible enough to adjust holding periods when fundamental cycle changes occur that alter the risk-reward characteristics of extended positioning.

What position size is appropriate for long term trading strategies?

Position sizes for long term trading should typically range from 1-3% of total account value per trade, with conservative sizing reflecting the extended capital commitment and psychological stress that multi-month holding periods create. Unlike shorter time-frame strategies, long term trading requires accounting for the increased emotional impact of holding significant positions through extended volatility periods that can test trader conviction despite intact institutional analysis. Smaller position sizes ensure that temporary adverse movements don't create psychological pressure that interferes with systematic cycle analysis.

The extended holding periods of long term trading justify conservative position sizing because successful institutional cycle analysis can generate 20-50% profits over 3-12 month periods, making smaller position sizes mathematically attractive when multiplied across multiple successful trades over time. Professional long term traders often prefer 1-2% position sizes that allow comfortable psychological management during extended holding periods rather than larger positions that might force premature exits during normal volatility that doesn't invalidate institutional cycle patterns.

How do you identify high-probability institutional cycles for long term trades?

High-probability institutional cycles for long term trading are characterized by convergence of multiple institutional factors including Federal Reserve policy direction, quarterly earnings trends, annual allocation cycles, and calendar-based rebalancing periods that create sustained directional pressure over extended periods. Professional traders look for situations where institutional incentives align across different time-frames rather than isolated factors that might create temporary price movements without sustained institutional commitment.

The best long term institutional cycles typically develop when policy cycles support institutional risk allocation while fundamental factors justify extended positioning and calendar patterns provide implementation timing that supports gradual institutional flows over months rather than immediate price adjustments. These convergences create mathematical edges that justify extended holding periods because institutional behavior becomes predictable across multiple decision-making cycles rather than depending on single events or temporary factors that might reverse quickly.

Can long term trading work during volatile market conditions?

Long term trading using institutional cycle timing can work effectively during volatile conditions when volatility reflects institutional transition periods rather than fundamental breakdown of institutional patterns that support extended positioning. Volatile markets often create optimal entry opportunities for long term trades when institutional cycles remain intact but short-term volatility creates temporary price dislocations that improve risk-reward ratios for extended holding strategies. The key is distinguishing between volatility that disrupts institutional patterns and volatility that creates positioning opportunities within intact cycles.

However, volatile conditions require modified position sizing and enhanced risk management because extended holding periods during volatile markets create increased psychological stress and larger drawdown potential that can interfere with systematic decision-making. Professional long term traders often reduce standard position sizes by 25-50% during volatile periods while maintaining systematic institutional cycle analysis, ensuring they can participate in genuine institutional trends while avoiding excessive stress during uncertain market phases that might extend longer than normal cycle timing suggests.

How do you manage long term positions when institutional cycles change?

When institutional cycles change during long term trades, positions should be evaluated systematically based on whether the changes invalidate the original institutional thesis or represent normal timing variations that don't affect the fundamental cycle pattern. Genuine institutional cycle changes typically involve Federal Reserve policy shifts, fundamental earnings trend reversals, or major allocation requirement changes that alter institutional behavior patterns fundamentally rather than temporarily delaying expected outcomes.

Professional long term traders establish specific institutional milestone criteria that trigger systematic position review, typically involving policy changes, allocation cycle completions, or fundamental pattern breaks that suggest institutional behavior has shifted permanently rather than experiencing temporary delays. The management approach often involves partial position reduction when institutional patterns show early change signals, preserving capital while maintaining exposure in case cycles resume their original patterns rather than changing permanently.

Resolution to the Problem

Long term trading when combined with institutional cycle timing solves the fundamental challenge that most traders face when attempting to capture extended market moves while maintaining systematic risk management throughout multi-month holding periods. Traditional long term investing approaches often lack the systematic framework necessary for optimal entry and exit timing, while shorter time-frame strategies miss the substantial profit opportunities that develop when institutional money flows create sustained directional trends over extended periods. Institutional cycle analysis provides the systematic foundation necessary for capturing these extended moves while maintaining risk management discipline.

The systematic nature of institutional cycle timing eliminates the emotional decision-making that typically destroys long term trading attempts when extended holding periods create psychological stress during normal market volatility. When long term positions are based on objective institutional cycle analysis rather than subjective market opinions, traders can maintain confidence in their systematic approach even during temporary adverse movements that don't invalidate the underlying institutional patterns. This mathematical foundation provides the psychological stability necessary for capturing the extended moves that make long term trading profitable.

Understanding that successful long term trading requires balancing extended profit capture with systematic risk management through institutional cycle analysis creates a framework for sustainable wealth building that compounds over multiple market cycles. The ability to position ahead of institutional flows while maintaining systematic exit criteria allows traders to optimize their capital allocation for the largest and most predictable market movements while preserving capital during inevitable periods when institutional patterns shift or experience timing delays that require position adjustment.

Join Market Turning Points

Master the sophisticated art of long term trading through Market Turning Points comprehensive institutional cycle analysis training program. Our systematic approach teaches you how to identify and capitalize on the extended institutional cycles that create the largest and most predictable market movements over multi-month periods. You'll learn to integrate Federal Reserve policy cycles with quarterly institutional patterns and annual allocation adjustments that drive sustained directional trends lasting 3-12 months rather than temporary price movements that reverse quickly.

Access our advanced training on multi time-frame cycle analysis, institutional flow timing, and systematic position management techniques that professional money managers use to capture extended market moves while maintaining strict risk management discipline throughout extended holding periods. Our members develop the analytical skills and emotional discipline necessary to position ahead of institutional decision-making cycles rather than reacting to price movements after professional money has already been allocated.

Join the Market Turning Points community and discover how professional traders combine institutional cycle timing with systematic risk management to create sustainable long term trading success. Our proven methodology provides the foundation for capturing the most substantial market movements while maintaining the psychological stability necessary for extended holding periods that separate successful long term traders from those who abandon positions during normal market volatility.

Conclusion

Long term trading when combined with institutional cycle timing represents the optimal approach for capturing the most substantial and predictable market movements while maintaining systematic risk management throughout extended holding periods. The convergence of Federal Reserve policy cycles, institutional allocation patterns, and calendar-based rebalancing periods creates mathematical edges that can be identified and exploited through systematic analysis rather than emotional market speculation. This approach transforms long term trading from hoping for favorable outcomes into positioning ahead of predictable institutional behavior that drives the largest market movements.

Professional implementation of institutional cycle timing for long term trading requires understanding how different institutional factors interact over extended periods to create sustained directional pressure that justifies multi-month holding strategies. The key insight is that successful long term trading comes from aligning with institutional decision-making cycles rather than attempting to predict market direction through technical analysis alone. This systematic approach creates sustainable competitive advantages that compound over multiple trading cycles while maintaining the risk management discipline necessary for long-term success.

The wealth-building potential of mastering long term trading through institutional cycle analysis becomes apparent as traders develop the ability to capture extended market moves while avoiding the emotional pitfalls that destroy most attempts at multi-month position management. Individual trades become more profitable when timing aligns with institutional cycles, while overall trading performance improves through systematic risk management that prevents premature exits during normal volatility that doesn't invalidate institutional patterns. This patient, systematic approach provides the foundation for substantial long term wealth accumulation that exceeds what shorter time-frame strategies can achieve.

Author, Steve Swanson