Institutional Swing Trading Timing: Track Calendar-Based Signals to Position Ahead of Major Market Turns

- Jul 26, 2025

- 14 min read

The difference between successful swing traders and those who consistently struggle isn't intelligence, capital, or access to information. It's timing. While most retail traders react to price movements after they've already occurred, institutional money operates on an entirely different schedule - one based on predictable calendar events that create systematic opportunities for those who understand the patterns.

Swing trading timing isn't about catching falling knives or trying to pick exact tops and bottoms. It's about recognizing that institutional money flows follow calendar-based cycles that repeat with remarkable consistency. Economic reporting dates, Federal Reserve meetings, quarterly rebalancing periods, and earnings seasons all create windows where smart money positions itself weeks before major market turns become obvious to everyone else.

At Market Turning Points, we've spent decades mapping these institutional timing patterns. We've discovered that successful swing trading timing comes from understanding when institutions accumulate, when they distribute, and how their scheduled activities create predictable market behavior. This isn't about predicting random market movements - it's about aligning yourself with the systematic approach that drives the majority of market volume.

When you master institutional swing trading timing, you stop gambling on price action and start positioning yourself alongside the money that actually moves markets. That's the foundation of consistent trading success.

The Calendar-Driven Nature of Institutional Money

Most retail traders think markets move randomly based on news, sentiment, or technical breakouts. But institutional money operates according to a strict schedule that has nothing to do with daily headlines. Large funds, pension plans, insurance companies, and hedge funds all follow calendar-based mandates that create predictable timing windows throughout the year.

Consider how a major pension fund operates. They don't make investment decisions based on daily market sentiment. Instead, they follow quarterly rebalancing schedules, annual allocation reviews, and regulatory reporting deadlines. These calendar obligations force them to buy and sell massive positions during specific time windows, regardless of short-term market conditions.

The same principle applies to hedge funds positioning around earnings announcements. They don't wait for companies to report their numbers - they analyze historical patterns, consensus estimates, and options pricing models weeks beforehand to determine optimal positioning. By the time earnings are announced, smart money has already established their positions and is simply waiting for volatility to create exit opportunities.

This calendar-driven approach extends to economic data releases, Federal Reserve meetings, and sector-specific events like oil inventory reports or pharmaceutical approval timelines. Each creates a predictable window where institutional activity spikes, providing timing opportunities for swing traders who understand the patterns.

The key insight is that institutional timing isn't random - it's systematic. Large money moves according to schedules, and those schedules create market opportunities that repeat with remarkable consistency throughout the year.

Why Economic Reporting Dates Create Predictable Patterns

Economic data releases represent the most reliable calendar-based timing signals available to swing traders. Employment reports, inflation data, GDP announcements, and Federal Reserve decisions all occur on predetermined schedules that institutional traders build their strategies around. Understanding these patterns is crucial for proper swing trading timing.

Take the monthly employment report as the clearest example. This data is released on the first Friday of every month at exactly 8:30 AM Eastern Time. But institutions don't wait for the announcement to position themselves. They begin analyzing leading indicators, survey data, and economic trends 2-3 weeks beforehand to anticipate the report's impact on interest rates, sector rotation, and currency movements.

The pattern is remarkably consistent. Institutional accumulation typically begins 10-15 trading days before major economic releases, reaches peak activity 5-7 days prior, and shifts to distribution mode immediately following the announcement. This creates specific timing windows where swing traders can position themselves alongside institutional flows rather than reacting to the eventual price movements.

Federal Reserve meetings follow an even more predictable pattern. With eight scheduled meetings per year, institutions have months to prepare their positioning strategies. They analyze Federal Reserve communications, inflation trends, and employment data to anticipate policy changes. The result is systematic accumulation ahead of meetings and programmed selling once policy decisions are announced.

These patterns repeat because the underlying institutional behavior doesn't change. Large funds operate according to risk management protocols that require them to position ahead of known volatility events. Understanding these timing requirements allows swing traders to anticipate institutional flows and position themselves accordingly.

The most successful swing trading timing strategies focus on the period 10-20 trading days before major economic releases. This is when institutional positioning is most active and before retail traders begin focusing on upcoming announcements.

Quarterly Rebalancing and Seasonal Money Flows

Quarterly portfolio rebalancing represents one of the most powerful timing patterns in institutional trading. Every three months, pension funds, insurance companies, and large investment managers are required to adjust their portfolios back to target allocations. This creates massive, predictable money flows that occur during specific calendar windows regardless of market conditions.

The timing is systematic and well-documented. Most institutional rebalancing occurs during the final five trading days of each quarter and the first three trading days of the new quarter. During these windows, trillions of dollars flow between asset classes based on mathematical formulas rather than market sentiment. This creates opportunities for swing traders who understand the mechanics.

Consider what happens when stocks outperform bonds during a quarter. By quarter-end, institutional portfolios become overweight equities and underweight fixed income relative to their target allocations. Rebalancing requirements force them to sell stocks and buy bonds to restore proper weightings. This selling pressure often creates temporary weakness in equity markets that has nothing to do with fundamental conditions.

The opposite occurs when bonds outperform stocks. Institutional selling of fixed income and buying of equities creates systematic support for stock prices during rebalancing windows. Understanding these flows allows swing traders to anticipate temporary price movements that occur for purely mechanical reasons.

Seasonal patterns extend beyond quarterly rebalancing to include year-end tax considerations, January portfolio reallocations, and summer liquidity patterns. Each creates timing opportunities for traders who understand when and why large money moves according to calendar requirements rather than market fundamentals.

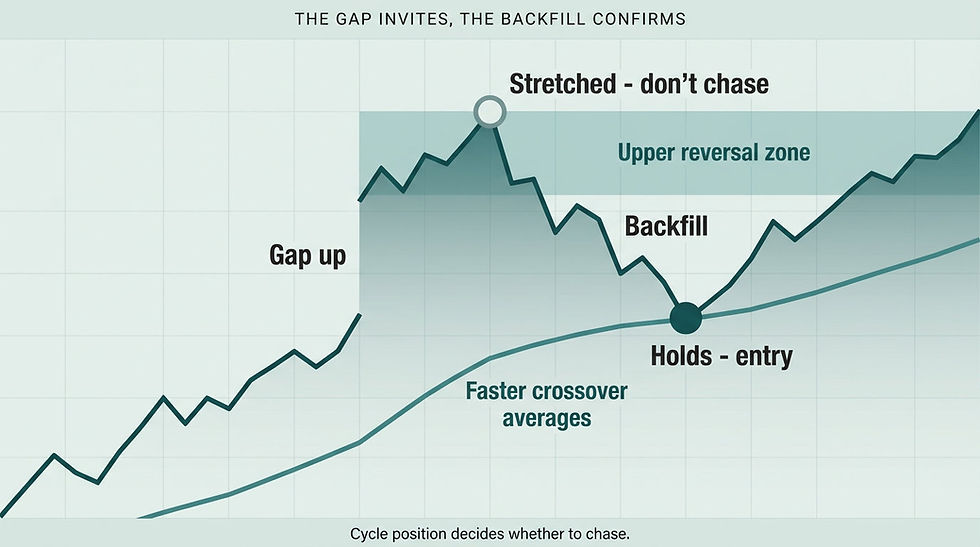

The key to successful rebalancing strategies is recognizing that these flows are non-discretionary. Institutions must rebalance regardless of market conditions, creating predictable timing windows that repeat every quarter with remarkable consistency. Understanding this timing becomes especially important when trading ETFs, as institutional flows into these instruments often create late-entry traps for retail traders who don't recognize the cyclical patterns. Check our post on Swing Trading ETFs with Cycle Timing: How to Avoid Late Entries Near Market Tops for more info.

Federal Reserve Meeting Cycles and Interest Rate Timing

Federal Reserve policy meetings represent the most important calendar-based timing events for swing traders. With eight scheduled meetings per year and additional emergency meetings when necessary, these gatherings create systematic volatility patterns that institutional money positions around months in advance.

The Federal Reserve operates on a transparent schedule published years ahead of time. This allows institutions to plan their positioning strategies around known policy dates rather than reacting to unexpected announcements. The result is predictable accumulation patterns that begin 6-8 weeks before meetings and systematic distribution that occurs immediately afterward.

Understanding Federal Reserve timing requires recognizing how different asset classes respond to policy expectations. Technology stocks, real estate investment trusts, and interest-sensitive sectors typically see institutional accumulation when rate cuts are anticipated. Conversely, financial stocks, energy companies, and cyclical sectors often experience buying pressure when rate increases are expected.

The timing pattern is remarkably consistent across different market cycles. Institutional positioning typically begins 30-40 trading days before Federal Reserve meetings, reaches peak activity 10-15 days prior, and shifts to profit-taking mode once policy decisions are announced. This creates specific windows where swing traders can align themselves with institutional flows.

Options markets provide additional timing insights around Federal Reserve meetings. Unusual activity in interest rate-sensitive sectors often appears 2-3 weeks before policy announcements, signaling institutional positioning that hasn't yet become apparent in stock prices. Understanding these early warning signals is crucial for optimal swing trading timing.

The most effective Federal Reserve timing strategies focus on the period immediately following policy announcements. Institutional selling pressure often creates temporary weakness in previously favored sectors, while new policy directions create accumulation opportunities in previously ignored areas of the market. However, it's important to remember that even during short-term market pullbacks, the underlying bullish cycle structure often remains intact, requiring traders to distinguish between temporary institutional profit-taking and genuine trend reversals. Check our post on Market Cycles Confirm Staying with Bullish Trends Despite Imminent Short-Term Pullbacks for more info.

Earnings Season Timing and Institutional Positioning

Earnings seasons occur four times per year on a predictable schedule that institutional traders plan around months in advance. Understanding how smart money positions around earnings announcements is crucial for swing trading timing, as these periods create systematic volatility patterns that extend far beyond individual company reports.

Institutional earnings strategies begin developing 4-6 weeks before reporting seasons start. Large funds analyze consensus estimates, historical volatility patterns, and options pricing to determine which sectors and individual stocks offer the best risk-adjusted opportunities. By the time earnings announcements begin, smart money has already established their core positions.

The timing pattern is systematic across different market cycles. Institutional accumulation typically peaks 2-3 weeks before earnings seasons begin, reaches maximum activity during the first week of reports, and shifts to distribution mode during the final week of the season. This creates predictable windows where swing traders can position themselves alongside institutional flows.

Sector rotation during earnings seasons follows predictable patterns based on reporting schedules and historical performance. Technology and growth sectors typically report early in the season, creating initial volatility that institutional money positions around. Financial and industrial sectors often report later, providing secondary timing opportunities as the season progresses.

Options markets provide crucial timing signals during earnings seasons. Unusual volume in specific strike prices and expiration dates often appears 10-15 days before individual companies report, indicating institutional positioning that hasn't yet become apparent in stock prices. Understanding these early warning signals allows swing traders to anticipate moves before they become obvious.

The most successful earnings timing strategies focus on sector-level opportunities rather than individual company bets. Institutional money flows during earnings seasons often create temporary dislocations between related stocks, providing swing trading opportunities that don't depend on specific company performance.

Volume Patterns and Institutional Accumulation Timing

Volume analysis provides one of the most reliable timing signals for swing traders because institutional money creates distinctive patterns that persist across different market cycles. Unlike retail trading, which tends to be reactive and emotional, institutional volume follows systematic patterns that reflect planned accumulation and distribution strategies.

Institutional accumulation creates specific volume signatures that trained observers can identify. Rather than sudden spikes that characterize retail buying, institutional accumulation typically shows gradual volume increases over 2-3 week periods. This reflects the systematic approach large funds use to build positions without moving prices significantly.

The timing of institutional volume patterns correlates strongly with calendar-based events. Volume accumulation often begins 15-20 trading days before major economic releases, reaches peak levels 5-10 days prior, and shifts to distribution patterns immediately following announcements. Understanding these timing relationships is crucial for optimal swing trading positioning.

Time-of-day volume analysis provides additional timing insights. Institutional trading typically concentrates during the first and last hours of trading when liquidity is highest. Unusual volume patterns during these periods, especially when they persist over multiple sessions, often signal institutional positioning that hasn't yet become apparent in price action.

The relationship between volume and price channels reveals institutional timing intentions. When volume increases during tests of channel boundaries without corresponding price breakouts, it often indicates institutional accumulation in preparation for larger moves. Conversely, volume spikes during channel breakouts typically signal that institutional positioning is complete and the move is beginning.

Cross-market volume analysis enhances timing precision by revealing institutional flows between related assets. When volume patterns in stock markets align with corresponding activity in options, futures, and sector ETFs, it confirms systematic institutional positioning rather than random trading activity.

Options Expiration Cycles and Strategic Timing

Options expiration cycles create some of the most predictable timing patterns available to swing traders. With monthly, weekly, and quarterly expirations occurring on predetermined schedules, these events generate systematic volatility and money flows that institutional traders position around weeks in advance.

Monthly options expirations on the third Friday of each month create the most significant timing patterns. Institutional strategies often involve complex positions that require unwinding or rolling into new contracts during expiration weeks. This creates predictable volume and volatility patterns that swing traders can anticipate and position around.

The timing mechanics are systematic and well-documented. Institutional activity typically increases 5-7 trading days before monthly expirations, reaches peak levels during expiration week, and shifts to new positioning immediately afterward. This creates specific windows where swing trading timing can be optimized based on expected institutional flows.

Quarterly options expirations amplify these patterns by concentrating institutional activity around specific dates. The simultaneous expiration of stock options, index options, and futures contracts creates what traders call "triple witching" - periods of increased volatility that institutional money positions around systematically.

Understanding options expiration timing requires recognizing how different strategies create predictable flows. Large institutional positions in covered calls often generate selling pressure as expirations approach, while protective put strategies create buying support during volatile periods. These flows occur regardless of fundamental conditions, creating timing opportunities for informed swing traders.

Weekly options expirations add another layer of timing complexity by creating more frequent volatility windows. While individual weekly expirations generate less institutional activity than monthly cycles, their cumulative effect creates ongoing timing opportunities for traders who understand the patterns.

The most effective options expiration timing strategies focus on the transition periods between expiration cycles. Institutional repositioning often occurs during the week following major expirations, creating temporary price dislocations that provide swing trading opportunities.

Cross-Market Timing Signals and Correlation Analysis

Institutional money doesn't operate in isolation - it flows systematically between related markets based on risk management requirements and strategic allocation decisions. Understanding these cross-market timing relationships is crucial for swing traders who want to anticipate institutional flows before they become apparent in individual assets.

Currency markets often provide the earliest timing signals for equity positioning. When institutions anticipate Federal Reserve policy changes or economic data releases, their initial positioning often occurs in foreign exchange markets before extending to stocks and bonds. Understanding these currency flows can provide 5-10 day advance warning of institutional equity positioning.

Bond market timing signals precede equity moves during periods of changing interest rate expectations. Institutional flows into or out of Treasury securities often indicate positioning for economic data releases or Federal Reserve meetings that will subsequently impact stock markets. These bond flows typically occur 1-2 weeks before corresponding equity moves become apparent.

Commodity markets provide timing signals for sector-specific institutional positioning. Oil price movements often precede energy sector rotation, while gold flows indicate institutional defensive positioning that extends to utilities and consumer staples. Understanding these commodity timing relationships helps swing traders anticipate sector rotation before it becomes obvious.

International market correlations reveal global institutional positioning that impacts U.S. markets with predictable timing lags. European market movements often precede corresponding U.S. sector rotation by 1-2 trading days, while Asian market flows provide overnight positioning signals for technology and growth sectors.

The key to successful cross-market timing analysis is recognizing that institutional money flows follow systematic risk management protocols. Rather than random movements between markets, these flows reflect coordinated positioning strategies that create predictable timing relationships across different asset classes. However, the ultimate profitability of swing trading depends not just on understanding these timing relationships, but on ensuring that cyclical analysis, precise timing, and favorable price levels all align before entering positions. Check our post on How Profitable is Swing Trading: Only When Cycles, Timing and Price Are Aligned for more info.

People Also Ask About Swing Trading Timing

What is the best time of day for swing trading timing?

Swing trading timing is most effective during institutional trading hours, particularly the first and last hours of the trading session when large money is most active. The opening hour (9:30-10:30 AM EST) often sees institutional positioning based on overnight developments and calendar events, while the closing hour (3:00-4:00 PM EST) reflects institutional adjustments and rebalancing activity.

However, swing trading timing focuses more on multi-day cycles and calendar-based patterns rather than intraday movements. The most important timing elements involve positioning 10-20 days before major economic releases and Federal Reserve meetings, when institutional accumulation typically begins. Daily timing becomes secondary to understanding these larger cyclical patterns.

How far in advance can institutional swing trading timing signals be detected?

Institutional swing trading timing signals typically appear 10-20 trading days before major market moves, depending on the type of calendar event. Federal Reserve meetings generate positioning signals 4-6 weeks in advance, while earnings seasons create institutional flows 2-3 weeks beforehand. Economic data releases usually show institutional positioning 1-2 weeks prior to announcements.

The key is understanding that institutional money operates on scheduled timelines rather than reactive patterns. Large funds must position themselves well ahead of known volatility events due to the size of their trades and risk management requirements. This systematic approach creates predictable timing windows that repeat with remarkable consistency across different market cycles.

Which calendar events provide the most reliable swing trading timing opportunities?

The most reliable swing trading timing opportunities occur around Federal Reserve meetings (8 times per year), monthly employment reports, quarterly earnings seasons, and quarterly portfolio rebalancing periods. These events create predictable institutional flows because they're scheduled far in advance and require systematic positioning by large funds.

Monthly inflation data and quarterly GDP releases also provide consistent timing patterns, though with somewhat less institutional activity. The key is focusing on events that institutions care about most - those that impact interest rates, economic growth, and sector allocation decisions. These calendar events create non-discretionary money flows that occur regardless of short-term market sentiment.

How do you identify institutional accumulation vs distribution timing?

Institutional accumulation timing typically shows gradual volume increases over 2-3 week periods before calendar events, often accompanied by subtle price strength during market weakness. This reflects the systematic approach large funds use to build positions without moving prices significantly, spreading their trades across multiple sessions to minimize market impact.

Distribution timing appears as volume spikes during or immediately after announcements, frequently with price weakness despite positive news. The key is recognizing that institutions position ahead of events (accumulation) and exit after events (distribution), creating predictable timing windows for swing traders who understand these patterns.

Can retail traders really time the market like institutions?

Retail traders can't match institutional resources, but they can succeed by following institutional timing patterns using cyclical analysis, price channels, and crossover signals. The key is recognizing that institutions create predictable timing footprints around calendar events rather than trying to compete with their analysis capabilities.

By focusing on systematic patterns and calendar-based cycles, retail swing traders can position themselves alongside institutional money flows rather than against them. This approach transforms timing from guesswork into a systematic methodology based on understanding when and why large money moves according to predetermined schedules.

Resolution to the Problem

The fundamental problem with most swing trading approaches is the lack of systematic timing. Retail traders typically react to price movements, news events, or technical signals without understanding the calendar-based patterns that drive institutional money flows. This reactive approach consistently puts them one step behind the money that actually moves markets.

The solution lies in understanding institutional swing trading timing through calendar-based analysis, cyclical patterns, and systematic positioning strategies. By recognizing when institutions accumulate ahead of Federal Reserve meetings, how quarterly rebalancing creates predictable flows, and why economic reporting dates generate systematic volatility, swing traders can position themselves alongside smart money rather than chasing moves after they occur.

Steve's methodology at Market Turning Points provides exactly this framework. Instead of reacting to price action or news events, we track the calendar-based patterns that drive institutional behavior. Our approach focuses on the timing relationships between scheduled events and institutional positioning, allowing subscribers to anticipate market moves rather than react to them.

Join Market Turning Points

If you're tired of missing market moves because you're always reacting instead of anticipating, it's time to learn institutional swing trading timing. Market Turning Points provides the calendar-based analysis, cyclical timing tools, and systematic approach you need to position yourself ahead of major market turns.

Our proprietary methodology identifies institutional timing patterns across multiple calendar cycles and market events. We teach you to recognize Federal Reserve positioning windows, quarterly rebalancing flows, and economic data timing patterns the way professional traders do. Most importantly, we provide real-time calendar analysis so you can anticipate institutional flows rather than chasing them after they've already moved prices.

You don't need institutional resources to benefit from institutional timing insights. Our systematic approach makes complex calendar analysis accessible to individual swing traders who want to improve their market timing and positioning consistency. Whether you're managing a retirement account or building trading capital, understanding institutional timing will transform your results.

To start mastering institutional swing trading timing and positioning yourself ahead of major market turns, join us today. You'll gain access to our calendar-based analysis, learn our systematic timing methodology, and discover how to turn institutional patterns into consistent trading advantages.

Conclusion

Successful swing trading timing isn't about predicting random market movements - it's about understanding the systematic, calendar-based patterns that drive institutional money flows. When you learn to recognize Federal Reserve cycles, quarterly rebalancing windows, and economic reporting patterns, you gain the same timing advantages that professional traders use every day.

The choice is simple: continue reacting to market moves after institutional money has already positioned itself, or learn to anticipate these moves by following calendar-based timing signals. Institutional patterns repeat consistently because the underlying behavior is systematic rather than random. Large funds still operate on scheduled timelines, still position ahead of known events, and still create detectable timing patterns in market data.

By mastering institutional swing trading timing, you transform trading from a reactive guessing game into a systematic approach with predictable timing advantages. That's the difference between hoping for good timing and creating it consistently.

Author, Steve Swanson